The new financial 2023-24 has just begun. There are tons of financial tasks for you to get started off with this time of the year. One of them is tax planning, and the sooner you get started on that one, the better.

The reason: You get to benefit from an additional 10 months’ worth of returns.

Tax saving benefits for investments are defined under Section 80C of the Income-tax Act. A variety of different investment products can fit under the 80C umbrella.

There are choices across insurance, pension funds, fixed deposits and equity investments that you can choose from within this tax saving incentive. However, not all the options make for a good investment. The smart way to utilise the 80C benefit is to keep one eye on the quality of the investment option too. For instance, insurance policies are not investments in their true form and fixed deposits offer only a five-year deposit option under this section and, hence, we are leaving these two out of the discussion and focusing on long-term wealth creation along with immediate tax saving via the remaining options.

Employees’ Provident Fund (EPF)

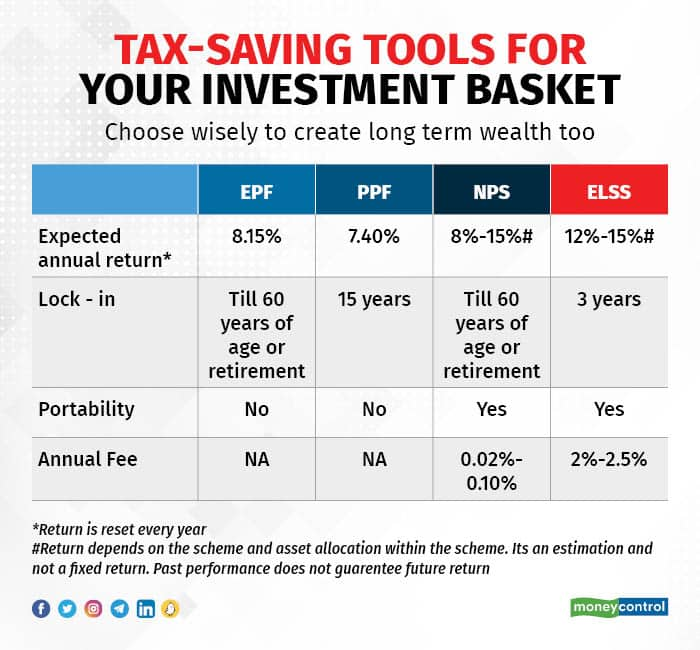

If your organisation is a member of the Employees’ Provident Fund Organisation (EPFO), then your total salary will consist of a pension component, where contribution is made by your employer and matched (voluntarily) by you. This is currently defined at 8.33 percent of basic salary. The contribution that you make from your net salary is allowed as a deduction for tax saving. Usually, this amount is linked to your basic salary and you don’t have control on the value. The total deduction is considered under Section 80C where the overall deduction limit is at Rs 1.5 lakh. If your EPF contribution for the year is less than this, you have room to add other investments.

According to Pratibha Girish, founder, Finwise Personal Finance Solutions, “For salaried clients, EPF is like a Secret Santa. If contributions are kept going through job changes, over the long term, returns compound and by the time one retires, it can contribute anywhere between 30 and 40 percent of the accumulated investment corpus.”

EPF is a forced saving that goes towards your overall long-term debt allocation and contributes significantly towards building that retirement corpus. At the present annual interest rate of 8.15 percent, this is a relatively high-return, low-risk investment.

Public Provident Fund (PPF)

PPF is accessible to anyone who would like to open an account and you can do so through your bank or your local post office. The advantage along with the tax deduction for the invested amount, under Section 80C, is the tax-free interest and tax-free maturity proceeds. This is, however, a 15-year locked-in investment and will fit into your long-term debt allocation.

PPF as an investment option was widely sought after around two decades ago when the annual interest rate on offer was in the range of 10-12 percent. Since then, the interest rate has steadily been revised lower and currently the annual interest rate is at 7.4 percent.

National Pension Scheme (NPS)

This is the newest offering in the pension investment segment. It’s a market-linked solution to a long-term wealth creation opportunity. An NPS contribution is treated similar to other eligible investments for deduction under Section 80C which is limited to Rs 1.5 lakh, aggregate. However, there is an additional deduction you can avail under Section 80 CCD for up to Rs 50,000 worth of contribution.

Being market-linked means you can choose to invest in different types of funds with a mix of equity and debt assets. Adding equity assets to the portfolio can improve the likelihood of earning inflation-beating post-tax returns over long periods. Ideally, you can choose an NPS scheme and keep adding your annual contribution for a decade or two and let the returns compound. The cost of this is very low and there is an additional tax advantage as the lump sum withdrawal (capped at 60 percent of the corpus) at retirement is also tax free.

Girish says, “While the additional Rs 50,000 investment with tax deduction for NPS should be encouraged as a savings tool, the forced annuity of 40 percent at retirement means you don’t have complete control over your money and the returns you can generate.”

A low-cost, market-linked, long-term retirement fund with enhanced tax advantage thanks to the additional Rs 50,000 deduction, it can enhance your corpus size and potentially deliver returns above long-term inflation.

Equity-linked Savings Scheme (ELSS)

These funds invest purely in equity and come with a minimum three-year lock-in. The tax deduction is similar to the others under Section 80 C. When you redeem you are liable to pay a long-term capital gains tax at 10 percent. If you can remain invested for at least 10 years, investing in equity is a very efficient way to earn compounded returns which beat inflation by a reasonable margin.

According to Amol Joshi, founder, Plan Rupee Investment Services, “Wealth creation happens through risk assets rather than fixed-return assets. This requires a shift in behaviour. A lot of debt allocation is already being taken care of thanks to provident fund investments. ELSS gives the required equity allocation and the flexibility with a low lock-in period.”

However, equity is a volatile asset and prices can fluctuate on a daily basis. The impact of compounding can only be felt by remaining invested for longer periods of time.

Girish says, “Starting an SIP (systematic investment plan) in a scheme of your choice at the beginning of the financial year helps put away small amounts rather than trying to put together a lump sum at the end of the year and also smoothens out market volatility.”

Last-minute investments towards tax savings can get chaotic and leave you little time to make the most efficient decision. Leaving it till the end means you’ll take up the most convenient option rather than choosing the investment tool that helps in long-term wealth creation. Tweak your process and start tax saving investments early in the financial year to squeeze maximum benefit along with a better alignment with your long-term investment plan.

|