[Under Section 45ZL of the Reserve Bank of India Act, 1934]

The fourth meeting of the Monetary Policy Committee (MPC), constituted under section 45ZB of the amended Reserve Bank of India Act, 1934, was held on April 5 and 6, 2017 at the Reserve Bank of India, Mumbai.

2. The meeting was attended by all the members - Dr. Chetan Ghate, Professor, Indian Statistical Institute; Dr. Pami Dua, Director, Delhi School of Economics; and Dr. Ravindra H. Dholakia, Professor, Indian Institute of Management, Ahmedabad; Dr. Michael Debabrata Patra, Executive Director (the officer of the Reserve Bank nominated by the Central Board under Section 45ZB(2)(c) of the Reserve Bank of India Act, 1934); Dr. Viral V. Acharya, Deputy Governor in-charge of monetary policy - and was chaired by Dr. Urjit R. Patel, Governor.

3. According to Section 45ZL of the amended Reserve Bank of India Act, 1934, the Reserve Bank shall publish, on the fourteenth day after every meeting of the Monetary Policy Committee, the minutes of the proceedings of the meeting which shall include the following, namely:–

(a) the resolution adopted at the meeting of the Monetary Policy Committee;

(b) the vote of each member of the Monetary Policy Committee, ascribed to such member, on resolution adopted in the said meeting; and

(c) the statement of each member of the Monetary Policy Committee under sub-section (11) of section 45ZI on the resolution adopted in the said meeting.

4. The MPC reviewed the surveys conducted by the Reserve Bank to gauge consumer confidence, households’ inflation expectations, corporate sector performance, credit conditions, the outlook for the industrial, services and infrastructure sectors, and the projections of professional forecasters. The Committee reviewed in detail staff’s macroeconomic projections, and alternative scenarios around various risks to the outlook. Drawing on the above and after extensive discussions on the stance of monetary policy, the MPC adopted the resolution that is set out below.

Resolution

5. On the basis of an assessment of the current and evolving macroeconomic situation at its meeting today, the Monetary Policy Committee (MPC) decided to:

- keep the policy repo rate under the liquidity adjustment facility (LAF) unchanged at 6.25 per cent.

6. Consequent upon the narrowing of the LAF corridor as elaborated in the accompanying Statement on Developmental and Regulatory Policies, the reverse repo rate under the LAF is at 6.0 per cent, and the marginal standing facility (MSF) rate and the Bank Rate are at 6.50 per cent.

7. The decision of the MPC is consistent with a neutral stance of monetary policy in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth. The main considerations underlying the decision are set out in the statement below.

Assessment

8. Since the MPC met in February 2017, indicators of global growth suggest signs of stronger activity in most advanced economies (AEs) and easing of recessionary conditions in commodity exporting large emerging market economies (EMEs). In the US, high frequency data indicate that the labour market, industrial production and retail sales are catalysing a recovery in Q1 of 2017 from a relatively subdued performance in the preceding quarter. Nonetheless, risks to higher growth have arisen from non-realisation or under-achievement of macroeconomic policies. In the Euro area, the manufacturing purchasing managers’ index (PMI) rose to a six-year high in March amidst improving consumer confidence and steadily strengthening employment conditions. In the Japanese economy, nascent signs of revival are evident in the form of falling unemployment, improving business sentiment on fixed investment, and rising exports helped by the depreciation of the yen; however, deflation risks linger.

9. For EMEs, the outlook is gradually improving, with indications that the slowdown characterising 2016 could be bottoming out. In China, supportive macroeconomic policies, surging credit growth and a booming property market have held up the momentum of growth albeit amidst concerns about financial stability and capital outflows. In Brazil, hardening commodity prices are providing tailwinds to reforms undertaken by the authorities to pull the economy out of recession, although financial fragilities remain a risk. Russia is benefiting from the firming up of crude prices and it is widely expected that growth will return to positive territory in 2017.

10. Inflation is edging up in AEs to or above target levels on the back of slowly diminishing slack, tighter labour markets and rising commodity prices. Among EMEs, Turkey and South Africa remain outliers in an otherwise generalised softening of inflation pressures. Global trade volumes are finally showing signs of improvement amidst shifts in terms of trade, with exports rising strongly in several EMEs as well as in some AEs whose currencies have depreciated.

11. International financial markets have been impacted by policy announcements in major AEs, geo-political events and country-specific factors. Equity markets in AEs were driven up by reflation trade, stronger incoming data and currency movements. Equity markets in EMEs had a mixed performance, reflecting domestic factors amidst a cautious return of investor appetite and capital flows. In the second half of March, dovish guidance on US monetary policy lifted equities across jurisdictions, especially in Asia, as the reach for EME assets resumed strongly, although doubts about the realisation of US policies, Brexit and softer crude prices tempered sentiments. Bond markets have mirrored the uncertainty surrounding the commitment to fiscal stimulus in the US and yields traded sideways in AEs, while they generally eased across EMEs. In the currency markets, the US dollar’s bull run lost steam by mid-March. EME currencies initially rose on optimism on the global outlook, but some of them have weakened in recent days with the fall in commodity prices. Crude prices touched a three-month low in March on rising shale output and US inventories. Food prices have been firming up globally, driven by cereals.

12. On the domestic front, the Central Statistics Office (CSO) released its second advance estimates for 2016-17 on February 28, placing India’s real GVA growth at 6.7 per cent for the year, down from 7 per cent in the first advance estimates released on January 6. Agriculture expanded robustly year-on-year after two consecutive years of sub-one per cent growth. In the industrial sector, there was a significant loss of momentum across all categories, barring electricity generation. The services sector also slowed, pulled down by trade, hotels, transport and communication as well as financial, real estate and professional services. Public administration, defence and other services cushioned this slowdown. To some extent, government expenditure made up for weakness in private consumption and capital formation.

13. Several indicators are pointing to a modest improvement in the macroeconomic outlook. Foodgrains production has touched an all-time high of 272 million tonnes, with record production of rice, wheat and pulses. The record production of wheat should boost procurement operations and economise on imports, which had recently surged. Rice stocks, which had depleted to close to the minimum buffer norm, have picked up with kharif procurement. The bumper production of pulses has helped in building up to the intended buffer stock (i.e., 20 lakh tonnes) and this will keep the price of pulses under check – the domestic price of pulses has already fallen below the minimum support price (MSP).

14. Industrial output, measured by the index of industrial production (IIP), recovered in January from a contraction in the previous month, helped by a broad-based turnaround in manufacturing as well as mining and quarrying. Capital goods production improved appreciably, although this largely reflected the waning of unfavourable base effects. Consumer non-durables continued, however, to contract for the second successive month in spite of supportive base effects. Thus, investment and rural consumption demand remain muted. The output of core industries moderated in February due to slowdown in production of all the components except coal. The manufacturing purchasing managers’ index (PMI) remained in expansion mode in February and rose to a five month high in March on the back of growth of new orders and output. The future output index also rose strongly on forecasts of pick-up in demand and the launch of new product lines. The 77th round of the Reserve Bank’s industrial outlook survey indicates that overall business sentiment is expected to improve in Q1 of 2017-18 on the back of a sharp pick up in both domestic and external demand. Coincident indicators such as exports and non-oil non-gold imports are indicative of a brighter outlook for industry, although the sizable under-utilisation of capacity in several industries could operate as a drag on investment.

15. Activity in the services sector appears to be improving as the constraining effects of demonetisation wear off. On the one hand, rural demand remains depressed as reflected in lower sales of two- and three-wheelers and fertiliser. On the other hand, high frequency indicators relating to railway traffic, telephone subscribers, foreign tourist arrivals, passenger car and commercial vehicles are regaining pace, thereby positioning the services sector on a rising trajectory. After three consecutive months of contraction, the services PMI for February and March emerged into the expansion zone on improvement in new business.

16. After moderating continuously over the last six months to a historic low, retail inflation measured by year-on-year changes in the consumer price index (CPI) turned up in February to 3.7 per cent. While food prices bottomed out at the preceding month’s level, base effects pushed up inflation in this category. Prices of sugar, fruits, meat, fish, milk and processed foods increased, generating a sizable jump in the momentum in the food group. In the fuel group, inflation increased as the continuous hardening of international prices lifted domestic prices of liquefied petroleum gas during December 2016 – February 2017. Kerosene prices have also been increasing since July with the programmed reduction of the subsidy. Adapting to the movements in these salient prices, both three months ahead and a year ahead households’ inflation expectations, which had dipped in the December round of the Reserve Bank’s survey, reversed in the latest round. Moreover, the survey reveals hardening of price expectations across product groups. The 77th round of the Reserve Bank’s industrial outlook survey indicates that pricing power is returning to corporates as profit margins get squeezed by input costs.

17. Excluding food and fuel, inflation moderated in February by 20 basis points to 4.8 per cent, essentially on transient and item-specific factors. In February, favourable base effects were at work in the clothing and bedding sub-group as well as in personal care and effects, the latter also influenced by the disinflation in gold prices. The volatility in crude oil prices and its lagged pass-through are impacting the trajectory of CPI inflation excluding food and fuel. Much of the impact of the fall of US $4.5 per barrel in international prices of crude since early February would feed into the CPI print in April as its cumulative pass-through occurred with a lag in the first week of this month. Importantly, inflation excluding food and fuel has exhibited persistence and has been significantly above headline inflation since September 2016.

18. With progressive remonetisation, the surplus liquidity in the banking system declined from a peak of 7,956 billion on January 4, 2017 to an average of 6,014 billion in February and further down to 4,806 billion in March. Currency in circulation expanded steadily during this period. Its impact on the liquidity overhang was, however, partly offset by a significant decline in cash balances of the Government up to mid-March which released liquidity into the system. Thereafter, the build-up of Government cash balances on account of advance tax payments and balance sheet adjustment by banks reduced surplus liquidity to 3,141 billion by end-March. Issuances of cash management bills (CMBs) under the market stabilisation scheme (MSS) ceased in mid-January and existing issues matured, with the consequent release of liquidity being absorbed primarily through variable rate reverse repo auctions of varying tenors. Accordingly, the average net absorption by the Reserve Bank increased from 2,002 billion in January to 4,483 billion in March. The weighted average call money rate (WACR) remained within the LAF corridor. The maturing of CMBs and reduced issuance of Treasury bills leading up to end-March has also contributed to Treasury bill rates being substantially below the policy rate.

19. Merchandise exports rose strongly in February 2017 from a subdued profile in the preceding months. Growth impulses were broad-based, with major contributors being engineering goods, petroleum products, iron ore, rice and chemicals. The surge in imports in January and February 2017 largely reflected the effect of the hardening of commodity prices such as crude oil and coal. Non-oil non-gold imports continued to grow at a modest pace, though capital goods imports remained sluggish. With imports outpacing exports, the trade deficit widened in January and February from its level a year ago, though it was lower on a cumulative basis for the period April-February 2016-17.

20. Balance of payments data for Q3 indicate that the current account deficit for the first three quarters of the financial year narrowed to 0.7 per cent of GDP, half of its level a year ago. For the year as a whole, the current account deficit is likely to remain muted at less than 1 per cent of GDP. Foreign direct investment (FDI) has dominated net capital inflows during April-December, with manufacturing, communication and financial services being the preferred sectors. Turbulence in global financial markets set off a bout of global risk aversion and flight to safe haven that caused net outflows of foreign portfolio investment (FPI) during November 2016 to January 2017. The tide reversed with the pricing in of the Fed’s normalisation path and improvement in global growth prospects. FPI flows turned positive in February and welled up into a surge in March, especially in debt markets relative to equity markets (which had been the dominant recipient until February). This reversal appears to have been driven by stable domestic inflation, better than expected domestic growth, encouraging corporate earnings, clarity on FPI taxation, pro-reform budget proposals and state election results. The level of foreign exchange reserves was US$ 369.9 billion on March 31, 2017.

Outlook

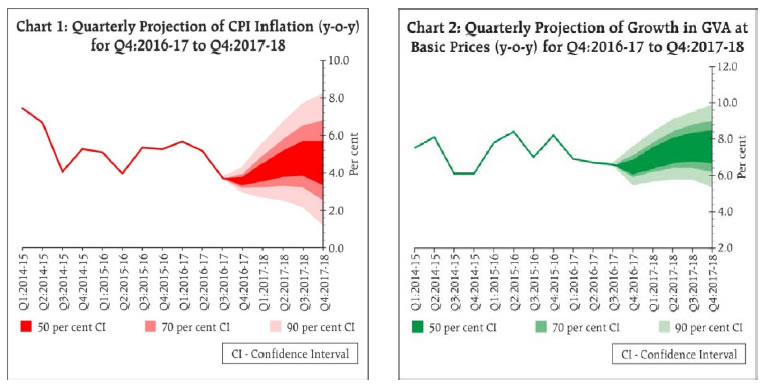

21. Since the February bi-monthly monetary policy statement, inflation has been quiescent. Headline CPI inflation is set to undershoot the target of 5.0 per cent for Q4 of 2016-17 in view of the sub-4 per cent readings for January and February. For 2017-18, inflation is projected to average 4.5 per cent in the first half of the year and 5 per cent in the second half (Chart 1).

22. Risks are evenly balanced around the inflation trajectory at the current juncture. There are upside risks to the baseline projection. The main one stems from the uncertainty surrounding the outcome of the south west monsoon in view of the rising probability of an El Niño event around July-August, and its implications for food inflation. Proactive supply management will play a critical role in staving off pressures on headline inflation. A prominent risk could emanate from managing the implementation of the allowances recommended by the 7th CPC. In case the increase in house rent allowance as recommended by the 7th CPC is awarded, it will push up the baseline trajectory by an estimated 100-150 basis points over a period of 12-18 months, with this initial statistical impact on the CPI followed up by second-order effects. Another upside risk arises from the one-off effects of the GST. The general government deficit, which is high by international comparison, poses yet another risk for the path of inflation, which is likely to be exacerbated by farm loan waivers. Recent global developments entail a reflation risk which may lift commodity prices further and pass through into domestic inflation. Moreover, geopolitical risks may induce global financial market volatility with attendant spillovers. On the downside, international crude prices have been easing recently and their pass-through to domestic prices of petroleum products should alleviate pressure on headline inflation. Also, stepped-up procurement operations in the wake of the record production of foodgrains will rebuild buffer stocks and mitigate food price stress, if it materialises.

23. GVA growth is projected to strengthen to 7.4 per cent in 2017-18 from 6.7 per cent in 2016-17, with risks evenly balanced (Chart 2).

24. Several favourable domestic factors are expected to drive this acceleration. First, the pace of remonetisation will continue to trigger a rebound in discretionary consumer spending. Activity in cash-intensive retail trade, hotels and restaurants, transportation and unorganised segments has largely been restored. Second, significant improvement in transmission of past policy rate reductions into banks’ lending rates post demonetisation should help encourage both consumption and investment demand of healthy corporations. Third, various proposals in the Union Budget should stimulate capital expenditure, rural demand, and social and physical infrastructure all of which would invigorate economic activity. Fourth, the imminent materialisation of structural reforms in the form of the roll-out of the GST, the institution of the Insolvency and Bankruptcy Code, and the abolition of the Foreign Investment Promotion Board will boost investor confidence and bring in efficiency gains. Fifth, the upsurge in initial public offerings in the primary capital market augurs well for investment and growth.

25. The global environment is improving, with global output and trade projected by multilateral agencies to gather momentum in 2017. Accordingly, external demand should support domestic growth. Downside risks to the projected growth path stem from the outturn of the south west monsoon; ebbing consumer optimism on the outlook for income, the general economic situation and employment as polled in the March 2017 round of the Reserve Bank’s consumer confidence survey; and, commodity prices, other than crude, hardening further.

26. Overall, the MPC’s considered judgement call to wait out the unravelling of the transitory effects of demonetisation has been broadly borne out. While these effects are still playing out, they are distinctly on the wane and should fade away by the Q4 of 2016-17. While inflation has ticked up in its latest reading, its path through 2017-18 appears uneven and challenged by upside risks and unfavourable base effects towards the second half of the year. Moreover, underlying inflation pressures persist, especially in prices of services. Input cost pressures are gradually bringing back pricing power to enterprises as demand conditions improve. The MPC remains committed to bringing headline inflation closer to 4.0 per cent on a durable basis and in a calibrated manner. Accordingly, inflation developments have to be closely and continuously monitored, with food price pressures kept in check so that inflation expectations can be re-anchored. At the same time, the output gap is gradually closing. Consequently, aggregate demand pressures could build up, with implications for the inflation trajectory.

27. Against this backdrop, the MPC decided to keep the policy rate unchanged in this review while persevering with a neutral stance. The future course of monetary policy will largely depend on incoming data on how macroeconomic conditions are evolving. Banks have reduced lending rates, although further scope for a more complete transmission of policy impulses remains, including for small savings/administered rates1. It is in this context that greater clarity about liquidity management is being provided, even as surplus liquidity is being steadily drained out. Along with rebalancing liquidity conditions, it will be the Reserve Bank’s endeavour to put the resolution of banks’ stressed assets on a firm footing and create congenial conditions for bank credit to revive and flow to productive sectors of the economy.

28. Six members voted in favour of the monetary policy decision. The minutes of the MPC’s meeting will be published by April 20, 2017.

29. The next meeting of the MPC is scheduled on June 6 and 7, 2017.

Voting on the Resolution to keep the policy repo rate unchanged at 6.25 per cent

| Member |

Vote |

| Dr. Chetan Ghate |

Yes |

| Dr. Pami Dua |

Yes |

| Dr. Ravindra H. Dholakia |

Yes |

| Dr. Michael Debabrata Patra |

Yes |

| Dr. Viral V. Acharya |

Yes |

| Dr. Urjit R. Patel |

Yes |

Statement by Dr. Chetan Ghate

30. Core inflation (CPI inflation excluding food and fuel) continues to be sticky, and its persistence poses upside risks for meeting the medium-term inflation target of 4 per cent within a band of +/- 2 per cent. Other exclusion based measures also remain elevated, although there have been transient declines in the demonetisation period. There has also been an inching up in the median 3 month and 1 year ahead inflationary expectations. The recent decline in headline inflation has been driven completely by food inflation and is likely to reverse in the summer months.

31. A strong upside risk to the inflation trajectory is the HRA implementation of the 7th Pay Commission. This needs to be watched carefully in terms of (i) to what extent the increase in the centre HRA is matched by state HRAs; and (ii) the extent to which the centre and state HRAs are implemented simultaneously (which means the inflationary effects will be stronger) or is staggered (which means the inflationary effect will be weaker). While we should see through any statistical effects from an increase in the HRA, the size of the second round effects may potentially be large depending on the extent and manner in which the HRA implementation takes place, in which case, there may be a need for a monetary policy response. Our focus on meeting the medium-term inflation target should remain laser sharp in light of such risks.

32. Since the last review, there is more clarity from both “soft” data (based on surveys), and “hard” data (based on actual economic performance), that the overall impact of demonetisation on the real economy has been transient. Importantly, the PMI in services has come out of contraction mode. The impact of demonetisation on Rabi sowing has also been very modest and transient – with a good monsoon and the strategic timing of the MSP helping in this regard. The performance of the real estate sector listed companies has seen an improvement. Large and medium industries have also recovered handsomely in terms of demand after demonetisation, although the small and micro sectors continue to be adversely affected. Overall, the output gap, while marginally negative, is closing gradually leading to the possible building up of inflationary pressures

33. As I mentioned in the last review, the pace of the ending of the re-investment of principal payments by the US Fed from its balance sheet holdings needs to be watched carefully, as also the extent to which such a “balance sheet reduction” by the Fed, as well as rises in the Fed funds rate, are disruptive for financial markets.

34. Taking into account these considerations, I vote for keeping the policy repo rate unchanged at 6.25 per cent at today’s meeting of the Monetary Policy Committee.

Statement by Dr. Pami Dua

35. Several factors indicate positive and modest growth in the economy. The remonetisation drive is progressing well, with the currency in circulation restored to almost 75 per cent of its value by end March of this year, which is expected to support discretionary spending. Spending in cash-intensive activities such as hotels, restaurants, transportation and the unorganised sectors is also on the rise. Further, a decrease in bank lending rates due to a delayed transmission of policy rate reductions in the past augurs well for the economy and may enhance consumption and investment spending. Various measures outlined in the Union Budget 2017-18 are conducive to growth in key sectors including the rural economy, infrastructure and housing, and are expected to have multiplier effects. The March 2017 round of the Industrial Outlook Survey undertaken by the Reserve Bank also shows improvement in sentiment in the corporate sector. On the external front, positive signs of growth across Advanced and Emerging Market Economies may boost demand for Indian exports. This optimism regarding domestic and global economic growth is also reflected in the leading indexes compiled by the Economic Cycle Research Institute (ECRI), New York.

36. On the inflation front, CPI inflation remained soft, primarily due to lower food prices, as vegetable prices declined, possibly due to distress sales as a result of demonetisation. However, core inflation (excluding food and fuel) continues to be higher, although it moderated slightly to 4.8 per cent in February. At the same time, upside risks to inflation remain, including remonetisation, rising rural wages, narrowing output gap, implementation of 7th CPC’s higher house rent allowances, rollout of GST, possibility of El Nino conditions, higher global commodity prices, uncertainty regarding prices of crude oil and exchange rate volatility. A Survey of Households Inflation Expectations undertaken by the Reserve Bank in March 2017 also indicates a rise in 3-month and 1-year ahead inflation expectations. Furthermore, ECRI’s Indian Future Inflation Gauge, a harbinger of Indian inflation, indicates some firming in inflation pressures.

Statement by Dr. Ravindra H. Dholakia

37. The effects of demonetisation on the Indian economy so far have turned out to be transitory and of lower magnitude vindicating our stand earlier. There are indications of a modest improvement in the domestic macroeconomic performance. The global outlook for growth, trade and prices has also improved. It is likely to have a favourable impact on Indian exports and the economy. The manufacturing purchasing managers’ index (PMI) and the Reserve Bank surveys also point to better sentiments on both the domestic and external demand. However, the capacity utilisation in industries has remained persistently low indicating at least continuing, if not widening, output gap. Against this, the headline inflation has been substantially below 4 per cent largely on account of vegetables and pulses. Inflation excluding food and fuel (core inflation) has been fairly sticky though has marginally declined to 4.8 per cent in February. Surplus liquidity in the economy since January 2017 has been steadily declining from 8 trillion to 4.8 trillion in March 2017.

38. The core inflation according to my calculations is likely to show a declining trend over the year. Moreover, the dynamics of pass-through from the non-core to the core inflation is changing such that volatility in the food/fuel prices would penetrate into core less easily than before. Oil prices according to me are not expected to stay high consistently. Simultaneous implementation of house rent allowances recommended by the 7th CPC by the Centre and all State governments is less likely and consequently its impact on inflation during 2017-18 may not be as high as 1 to 1.5 percentage points. The rising probability of El Nino event around July-August may adversely affect food production but may not seriously impact the food prices in view of comfortable buffer stocks. The GST implementation may not substantially impact the headline inflation because of multi-tier rate system.

39. In view of all this, the inflation projection according to my calculations is an average of around 4 per cent for the first half of 2017-18 and around 4.5 per cent for the second half of the year. Given the surplus liquidity still floating in the system, any change in the policy rate is not desirable at this stage. The liquidity position is expected to return to the normal level consistent with the neutral stance soon.

Statement by Dr. Michael Debabrata Patra

40. True to projections made at the time of the last meeting of the Committee, inflation is turning up. It seems to me that it is coming out of the U-shaped compression imposed by demonetisation and is now positioned on the rising slope. Several factors merit pre-emptive concern.

41. First, just as it drove a disinflation that started in August – well before demonetisation, which is responsible only for the sub-4 per cent trough – it is food that has pushed up headline inflation in February. And it is not the usual suspect – vegetables. It is the more sinister elements – protein-rich items other than pulses; cereals; sugar. When inflation rears its ugly head in these items, experience suggests it is likely to stay.

42. Second, inflation excluding food and fuel has been unrelenting. It is only in the February reading that there is a small downward movement, but is it sustainable? I think not: it is item-specific rather than generalised. If staff's projection are indicative, inflation excluding food and fuel will probably run ahead of headline inflation throughout 2017-18.

43. The consequence of the firming up of these salient prices is that inflation expectations have reversed and hardened, and not just in the near term but also a year ahead and across all product groups. Consumer confidence in the price situation has deteriorated. Firms are regaining pricing power.

44. Third, high frequency indicators may be indicating that demonetisation affected actual output rather than potential. With remonetisation, therefore, the output gap may close sooner than expected – perhaps at a sub-optimal level since there is slack in several industries – and demand pressures could soon confront the path of inflation in the months ahead.

45. These developments suggest to me that momentum is gathering underneath inflation developments, which appear benign at this juncture. In the second half of 2017-18, favourable base effects fade, and if food inflation rises alongside the stickiness in underlying inflation, it could become a perfect storm.

46. So much for the ingredients of inflation. Let me turn to costs.

47. The most important cost push will emanate from the 7th pay commission's house rent allowance. The first order statistical impact on the CPI may take headline inflation to or beyond the upper tolerance band. Second order effects will work through expectations and ‘Deusenberry effects’ as it spreads to states, PSUs, universities, and onwards. These effects will occur on top of the first order effect and 6 per cent plus inflation could be here to stay for some time.

48. The second one is the one off effect of the GST - small relative to the 7th pay commission and short lived, it could still last a year and push up inflation.

49. Third, several administered price elements are being adjusted upwards – milk; gas; kerosene; the MSP, as usual – and they will take their toll on headline inflation.

50. Finally, let me turn to the elephants in the room, keeping in mind that whether elephants fight or play, the grass suffers.

51. Closest to home is the south west monsoon. The probability of an El Niño event is rising and if food inflation gets entrenched as it did in 2009 in the trail of a sub-normal monsoon, there will be second order effects.

52. The second one is imported inflation, including through bouts of financial market turbulence and the rising tide of protectionism.

53. The third is global inflation – mercury is rising across advanced economies and it cannot be that India will be immune to it. Normalisation of monetary policy has begun in those economies, and it is not just the raising of policy rates/short-term rates. Normalising overly distended balance sheets can produce tightening of longer rates as well.

54. To sum up, I believe that a pre-emptive 25 basis points increase in the policy rate now will point us better at the target of 4 per cent to which the Committee has committed explicitly. It will also obviate the need for back-loaded policy action later when inflation is unacceptably high and entrenched. On balance, however, I vote for holding the policy rate unchanged in this bi-monthly meeting and await a few more readings of incoming data so that remaining transitory factors have passed and a clearer assessment of domestic and global macroeconomic conditions emerges.

Statement by Dr. Viral V. Acharya

55. Headline inflation is set to rebound from its recent lows due to the expected (and in the past month, realized) mean-reversion in food inflation, especially in vegetables. Global inflationary trends have remained on the upside too. There is some uncertainty as to when the headline inflation might cross the target inflation rate of 4 per cent and keep inching above, given that inflation without food and fuel is stubbornly above the target rate. We have laid out in the resolution several upside risks, of which geopolitical risks and undoing of the center’s fiscal discipline by the states concern me the most. Commodity prices, especially crude, have been volatile and so has the exchange rate. Hence, risks are evenly balanced around the inflation outlook.

56. On the growth front, the remonetisation is continuing apace and many sectors of the economy are recovering steadily after the transient slowdown. There are signs though that the recovery is somewhat uneven. Private investment, given the high indebtedness of several stressed sectors, remains a particularly weak spot. Household expectations of income, spending and employment appear to have weakened, but may be anchored to the past few months and need to be tracked in the coming months. Other signs of economic activity paint a rosier picture for the growth over the next year, with the external sector having been remarkably resilient.

57. Should an inflation-targeting central bank react to a narrowing output gap in such a scenario? Given the balanced nature of risks and uncertainty that abounds, I lean towards continuing the neutral stance and pause for now. There are many important issues to attend to, notably (i) resolving bank stressed assets and correcting weak bank balance-sheets; (ii) mopping up in a more durable manner the surplus liquidity sloshing around post-demonetisation and which is keeping short-term money market rates away from the policy rate; and (iii) unleashing the true potential of our capital markets further, by enhancing liquidity in the corporate bond market, and improving the ease and the suite of financial hedging options. It seems an opportune time to focus on these issues.

Statement by Dr. Urjit R. Patel

58. After reaching a historic low in January 2017, CPI inflation in February 2017 edged up, as expected. However, in all probability, inflation will significantly undershoot the 5 per cent target set for Q4 of 2016-17. Vegetable prices, which had declined sharply during November 2016 to January 2017, seem to have stabilised but may go up in the coming months due to a seasonal pick up. CPI inflation excluding food and fuel remained sticky, especially services. Also, given the volatility in the CPI, it is not easy to read its evolution. The outlook for inflation faces several other risks. Input costs have been rising, which could be passed on to output prices as demand strengthens. Further, the implementation of the HRA allowances recommended as part of the 7th CPC and the GST are risks, which could alter the inflation outturn in 2017-18. Uncertainty about the crude oil price trajectory is both ways given recent movements. Heightened geo-political risks continue to impart financial volatility in global markets.

59. The latest data released by the CSO suggested that the impact of demonetisation on economic activity was modest. Economic activity is expected to pick up in 2017-18, although there is the usual uncertainty about the monsoon at this stage. Several lead indicators suggest some improvement in the economic outlook. The industrial outlook survey of the Reserve Bank suggests positive outlook for the manufacturing sector. However, investment activity continues to be weak, but which is unsurprising given the headroom with respect to capacity utilisation in industry (Reserve Bank surveys).

60. Demonetisation induced liquidity facilitated faster monetary transmission. There is still room for banks to cut lending rates. For efficient transmission, it is important that interest rates on small savings are not out of line with interest rates on other comparable instruments in the financial system.

61. Notwithstanding likely favourable base-effects in the next few months, the outlook for inflation calls for close vigilance with a view to ensuring that the medium-term inflation trajectory evolves in line with the objective of bringing headline inflation closer to 4.0 per cent on a durable basis and in a calibrated manner. Therefore, I vote for maintaining the status quo in both the policy repo rate, and the stance.

Ajit Prasad

Assistant Adviser

Press Release : 2016-2017/2844

|