Shri N. S. Venkatesh, Executive Director, IDBI Bank & Chairman, FIMMDA, Shri B. Prasanna, Chairman PDAI, senior colleagues from the banking fraternity, delegates from India & UK, ladies and gentlemen. It is my pleasure to be part of the Annual FIMMDA-PDAI Conference being held in one of the leading financial centres of the world. London is home of one of the world’s oldest central banks and epitomizes the intellectual churning that has happened internationally about the role of central banks in the regulation of the financial sector. From being a poster boy of the philosophy of central bank being divested of all other responsibilities other than monetary policy, before the crisis, to the restorer of central bank primacy in financial regulation, the experience of London, the pre-eminent financial centre, offers valuable lessons for other countries. Going through the rich and intellectually riveting debates in the House of Commons and the House of Lords on the Financial Services Bill, which was enacted in December 2012, is an across the spectrum study in the philosophy of financial regulation.

2. I have been associated with the area of market regulation long enough to have mulled and struggled with different strands of the philosophy of regulation as it has evolved over the past few decades. The financial sector in India has developed over the years in the context of varying politico-economic considerations at different points of time. The program of economic reforms initiated in the nineties was a seminal point in India’s economic history. For billion Indians, this was nothing short of revolution, opening huge opportunities. Due to these reforms, we broke the shackles of low growth and recorded impressive growth rates. India’s entry in to the league of top economies of the world and a preferred investment destination validated the success of the policy.

3. These changes were result of well-thought policies. Though the push can be attributed to the precarious economic situation of 1991, the course was set by series of calibrated steps. Reforms were carried out keeping in view the interests of all the stakeholders, especially large sections that are economically weak. Steady reforms have proved to be more stable and durable.

4. Financial sector reforms have been part of overall scheme of reforms and have complemented the other components of economic policy. One notable feature of financial sector reforms in India since they were instituted in the early 1990s has been the maintenance of financial stability through a period marked by repeated financial crises across the world. Our financial markets have emerged stronger; became deep and liquid during this period. They also became more resilient in wake of challenging domestic and global events.

5. Our approach to “market regulation” all these years has evolved keeping the systemic imperatives and institutional prudence at the center. The pace of progress may have varied and, at times, discontinuous but that has more to do with the uncertain macro environment. Policymaking can never be a linear, uni-dimensional process unless it is ideological, which ours is not. But in terms of final outcomes, we have covered a tremendous distance. I have in the past talked about what have been the key attributes and achievements of our approach, so would not want to repeat that. I would just mention that our approach has never been statist and the import of a lot of small things being discussed and implemented does not fully register in the wider deliberations amid the din of absolutist arguments.

6. Since we began the financial sector reforms, Indian bond markets have come a long way. Bond market activity has grown rapidly. Government securities market (G-Sec), corporate bond market and derivatives markets have become broad-based in terms of participation. The debt and derivatives products that are available have grown in number and complexity. The sovereign yield curve now spans up to 40 years. Primary market issuances have increased resulting in large benchmark issuances. The volumes in secondary market have surged. The bid-ask spread of on-the-run securities continues to be low and so are impact costs. In case of corporate bonds too, trading volumes have increased but lag in comparison with global peers.

7. There have been significant changes in market micro-structure and infrastructure. Over the period of past two decades, the Reserve Bank of India has adopted a strategy for creation of an efficient market infrastructure to enable safe trading, clearing and settlement. State-of-the-art primary issuance process with electronic bidding and straight-through-processing (STP) capabilities, an efficient, completely dematerialized depository system within the central bank, Delivery-versus-Payment (DvP) mode of settlement, Real Time Gross Settlement (RTGS), electronic trading platform (Negotiated Dealing Systems - Order Matching) (NDS-OM) and a separate Central Counter Party (CCP) in the Clearing Corporation of India Ltd (CCIL) for guaranteed settlement are among the steps that were taken by the Reserve Bank over the years. The system makes G-Sec trading practically risk free and efficient.

8. Today, I would try to present the big picture emerging a few years from now as many of the small pieces we are currently pursuing finally coalesce into the larger theme. Both as a result of studied re-assessments within as well as convergence with globally accepted best principles several far-reaching initiatives have been announced in the recent past. It may, however, be contextual to understand the underpinnings of this process, at times criticized of not being able to deliver.

The Critique and the Response

9. The state of markets and market regulation in India has been often criticized for not achieving an efficient bond-currency-derivatives (BCD) nexus. A seemingly logical but misleading conclusion drawn from this is that the current institutional structure is to be blamed for this. The argument is that by changing the institutional structure, by itself, would succeed in reversing the public policy consensus relating to financial markets. This is at best a very facetious argument and completely belies the shared views among all the regulators and the Government regarding the broad philosophy and objective of financial sector policies.

10. The other fallacy is to believe that BCD nexus can be enforced only through exchanges, which perhaps is an extension of the earlier argument. While it is true that exchanges play an extremely important role in furthering development of efficient markets and price discovery, and more importantly address counterparty risk issues which are there in the OTC market, much of the risk transfer in the most developed markets happens in the OTC market among large institutional players. With the post crisis focus this segment has received, many of the earlier weaknesses have been addressed.

11. While the phrase ‘BCD Nexus’ sounds intellectually impressive, what it simply means is that there are certain restrictions regarding participation of various economic entities in the currency and interest rate markets and the related derivatives. Yes, there indeed these markets are tightly regulated. But what is the underlying philosophy behind these regulations? Instead of talking about market regulation in abstractions, it would be useful to understand what it actually entails.

12. Let us take currency markets. The markets have traditionally been OTC, seeking to cater to the genuine hedging needs of the entities. Given the capital account management framework, obviously there are guidelines of who can participate in what kind of products. These guidelines have been significantly liberalized over the years and newer products have been introduced on the exchanges. Now, the question here is at what stage do we move to a completely open capital account which would, in turn, result in freeing up the restrictions on participation in these markets. The latter follows from the first, not the other way round. This is institutional-structure agnostic.

13. Another structural factor with regard to an efficient BCD nexus is the nature of institutional market. In a bank-centric financial system, it has been the experience that even the task of developing non-bank channels, particularly through market-based mechanisms, falls ultimately on the banks themselves. Whether it is expecting banks to provide credit enhancement for bond markets or acting as market-makers in various market segments, the role of banks becomes critical. This reflects the underlying structural makeup of the financial system and implies that any attempt at relaxing market regulation ultimately comes unstuck at the altar of prudential regulation. The same, to a lesser extent, applies to other regulated entities as well, such as, insurance companies, pension funds, etc. which are seen as natural participants in some market segments, such as, corporate bonds, interest rate derivatives, credit default swaps but the prudential regulatory framework, perhaps for very valid reasons, is more conservative. Again, it is a matter of regulatory philosophy than the institutional structure.

14. As regard debt markets, the regulations essentially entail specification of broad product features and participation norms. While the considerations behind regulating interest rate markets are different form exchange rate markets, the objective still remains systemic stability. Large sovereign borrowings impact the yield curve through the expectation channel. Apart from direct balance sheet effects on the financial sector, interest rate volatility has a critical bearing on sovereign balance sheet which could translate onto financial sector balance sheets. It, therefore, becomes imperative to be watchful of volatility in interest rates on account of activities of various market players.

15. Active, unfettered repo market is one of the critical elements of such BCD construct. Repo markets were one of the most active funding markets globally before the crisis. Post-crisis, however, several work-streams under FSB, IOSCO, etc. are working internationally to tighten the regulation of repo markets, including regulations on re-use of securities, margins and haircuts, leverage built-up through repo markets, etc. These are not market conduct issues but prudential issues, being discussed in the context of systemic stability.

16. Market regulation cannot remain a value-neutral term. Different markets have different dynamics and inter-connections with the real sector and broader macroeconomic stability. To argue that regulation of equity markets is same as regulation of currency markets is facetious, ignoring the massive work going on internationally towards reforming the financial sector. Yes market mechanics can be same and market micro-structure can be convergent across asset classes but in terms of systemic spillover, approach to regulation of these markets can be very different.

17. So the point I am trying to make is that the debate needs to be on the nature of financial regulation and the underlying structural imperatives rather than the institutional structure. Various models have been tried internationally pre-crisis and post-crisis and it’s the contextual imperatives which have driven the changes.

The Path Ahead

18. Planning towards future, I can cite the policy direction provided by our Governor Dr. Raghuram Rajan. While talking about the Five Pillars of RBI's Developmental Measures, Dr. Rajan identified 'broadening and deepening financial markets and increasing their liquidity and resilience' as an important pillar. The objective is to help allocate and absorb the risks entailed in financing India’s growth. He had observed that markets are complementary to development of banking sector. The tasks ahead are:

-

Building liquidity and improving market access;

-

Developing Government bond market domestically in terms of investor class, instruments, infrastructure, intermediaries and innovations and opening up to foreign investors in a calibrated manner to broaden the investors’ base without unduly exposing it to the risks of sudden stops; and

-

Better communication of the debt management policy to avoid uncertainty in the minds of investors.

19. Going forward, by the year 2020, I would expect macro-economic management to become more robust, large scale fiscal consolidation resulting in optimal debt structure, bond markets becoming more liquid and deep, host of reforms in derivatives space and central bank communication becoming more robust and effective. I would like to share some of my thoughts on the issues.

I. Debt Management: Medium Term Debt Strategy

20. Recently we have articulated, in consultation with the Government, our medium term debt management strategy (MTDS). The move was designed to benchmark our debt management practices with global sound practice and foster transparency and accountability. MTDS comprises objectives, various benchmarks and portfolio indicators and yearly issuance strategy (external and domestic funding, instruments, maturity structure, etc.). It provides requisite information, transparency & certainty and enables market participants (investors) to plan their strategy for investment in Government bonds market.

21. The MTDS has been articulated for a period of three years and it will be reviewed annually and rolled over for the next three years. The scope of debt management strategy is presently limited to active elements of domestic debt management, i.e., marketable debt of the Central Government only. Over time, the scope would be progressively expanded to cover the entire stock of outstanding liabilities including external debt as well as General Government Debt including State Development Loans (SDL).

22. The debt management strategy revolves around three broad pillars, viz., borrowing at low cost over a period of time, risk mitigation and market development. The intended process as part of MTDS entails the following:

-

Carrying forward transparent issuance process by providing clear information on borrowing programme to investors and having continuous investor interactions and appropriate consultation;

-

Building up benchmark issues by issuing significant volumes and taking advantage of liquidity premia;

-

Elongating the maturity of the debt portfolio;

-

Building a balanced maturity profile and supply along the yield curve;

-

Issuing a variety of instruments, such as, inflation linked bonds that would help the investors to manage their portfolio more efficiently;

-

Undertaking switches / buybacks for effective liability management;

-

Expanding the domestic investor base by encouraging retail and mid-segment investors’ participation in G-Sec market and calibrated opening of the government securities market to foreign investors and retail investors; and

-

Continuing passive consolidation with large benchmark issuances and active consolidation through buy-backs / switches/ conversions.

23. An important risk mitigation measure aimed at alleviating the pressure at short-end was undertaking switches/buybacks from proximate maturities in order to reduce the redemption concentration and create space for further issuances that may be needed to meet the demand of market participants. During the past three fiscal years, switches amounting to about Rupees one trillion were undertaken by the Reserve Bank in consultation with the Government. The operations have eased gross borrowing numbers and enabled effective borrowings.

24. The aim of the Reserve Bank has always been to conduct market borrowing operations in a smooth manner without undue disruptions. The strategic and tactical approaches of debt management are meant to ensure the same. While the strategic parameters are set in MTDS and anchored to achieving the main objectives, the tactics are not only linked to the objectives but also to ensuring stability of operations. A recent example would bring out this approach. The market participants were expressing apprehensions about the potential elevated supply of government bonds due to the issuances by the state governments under Ujwal DISCOM Assurance Yojana (UDAY).

25. The yields had hardened in anticipation, especially for state government borrowings. We have acted in a calibrated manner planning issuances to banks that have DISCOM dues directly so that the supply will not enter the market. Selective regulatory forbearance of categorizing the bonds as ‘HTM’ was accorded to subscribing banks. The bonds issued to pay dues to the central public sector undertakings were offered through private placements. The pressure on the yields also moderated by modulating the issuance strategy to limit issuances at long tenors announcing the same in the borrowing calendar for first half of the fiscal 2016-17. This was possible because we had over time elongated the maturity profile of the Government bonds; weighted average maturity of 10.50 years as on end-March 2016 is one of the highest among the peers. This flattened the yield curve bringing down yields at 15 years and above, thereby increasing attractiveness of the state bonds issued under UDAY.

26. The timing of issuances was planned keeping in view absence of supply at end of fiscal year. The issuances were successful and UDAY bonds of about ₹ 990 billion were successfully placed. The Fixed Income and Money Market Dealers Association (FIMMDA) played an important role here in co-ordinating with banks for smooth issuances. The market behavior in this case, however, bears scrutiny. The markets exhibited serious negativity, mostly as a response to imaginary stress. There is also evidence of uni-directional bias, i.e., the market was unduly pessimistic impacting yields. It also brings forth need for better communication from the issuers. There are lessons to be learnt from the episode.

II. Secondary Market Trading

Enhancing liquidity of the debt market

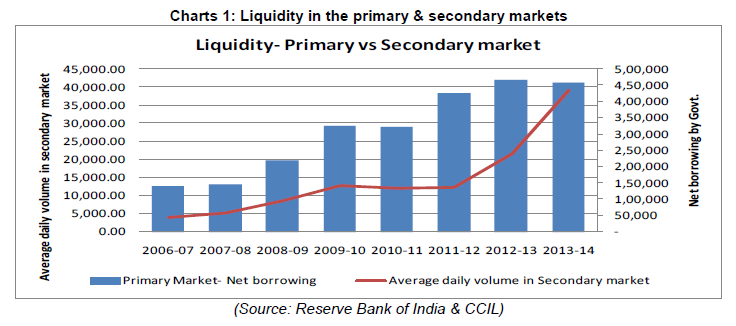

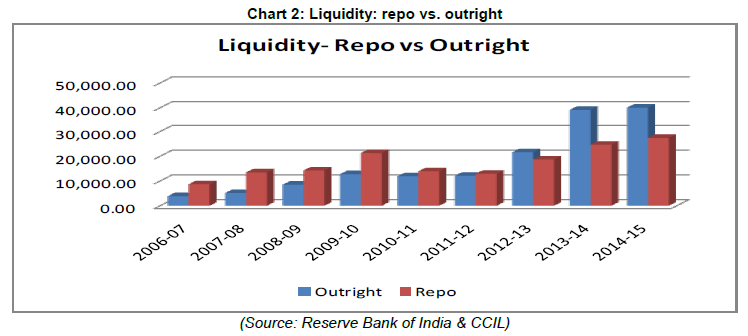

27. In the recent past, concerns have been raised globally about both a decline in current market liquidity, especially for fixed-income assets, and its resilience, as brought out in the IMF Global Financial Stability Report, 2015. In this context, it may be mentioned that liquidity in the Indian G-Sec markets, as indicated by trading volumes, improved significantly across markets alongwith increase in net borrowing. One of the reasons for the improved liquidity in G-sec and Repo is due to the electronic platform based trading (Charts 1 & 2).

28. The above was also borne out by a study undertaken by the Centre for Advanced Financial Research & Learning (CAFRAL) which found a strong positive impact on market efficiency through the introduction of NDS-OM and its associated transformational impact in the secondary market for government bonds, namely:

-

Ten-fold rise in daily trading volume;

-

The enormous shift to NDS-OM platform at the expense of OTC brokered sub-market;

-

Lower trade execution search costs; and

-

Real-time reporting of trade book and order book information leading to real time public dissemination as well.

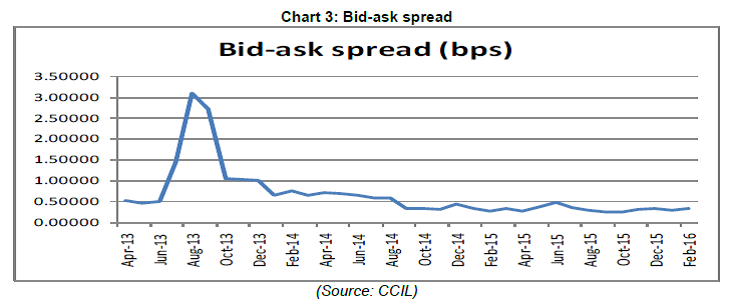

29. Liquidity as measured by bid-ask spread shows that market liquidity dried up in second half of 2013. Market volumes, however, remained high. Since then, the bid-ask spread has compressed significantly suggesting improvement in liquidity (Chart 3).

30. Various measures have been taken to enhance the secondary market liquidity in Government bond market. Consequently, the average daily trading volume has increased more than six times in the last five years. During the taper tantrum, investors could exercise the option to sell securities in an orderly fashion and exit without market disruption. This improved credibility of Indian markets and the investors returned. We have tweaked short-sale limits, opened ‘when issued’ market and started buy-back operations based on the cash position of government. We have initiated switches that would ease redemption pressure as well as aid consolidation. We are also discussing with the Government a suitable market making scheme for illiquid and semi-liquid Government securities. There is, however, work still to be done.

III. NDS-OM Version 2 Enhancements

31. NDS-OM, RBI’s Anonymous Order Matching System for dealing in secondary market outright trades in G-Sec was launched in August 2005 based on an internal assessment of the need for a screen based dealing system as recommended by the R. H. Patil Committee appointed by Reserve Bank of India. All trades concluded on NDS-OM flow within an STP framework to the CCIL, which acts as the CCP for all these trades, within the provisions of its bye-laws, rules and regulations.

32. From a relatively simple system when initially launched in August 2005, over time various functionalities have been added to NDS-OM. The application facilitates trading in all kinds of Central Government/State Government/Treasury Bill instrument in standard and non-standard (odd) market lots. It also facilitates trading in “When Issued” (both re-issues and new issues). Other important system capabilities include short-selling and limit monitoring, stock balance monitoring, ‘When Issued’ limit monitoring, web-based module for client dealing, etc. The system has been widely accepted by market participants and its order matching segment now consistently accounts for 80 - 85 per cent of total G-Sec market volumes. The average daily volumes on NDS-OM have increased from ₹ 50 billion in -2005-06 to over ₹ 400 billion in 2015-16.

33. As part of vision of the Reserve Bank of India for providing state-of-the-art infrastructure to market participants, Reserve Bank has initiated an upgradation of the NDS-OM platform. The new system is expected to have faster through-put, enhanced functionalities, rich user interface, internationally compatible message formats, etc.

Access of demat account holders to NDS-OM

34. One of the major factors said to be hampering trading interest in G-Sec is the difficulty in access to NDS-OM by non-institutional investor class. There is the gilt-account route but a large number of investors holding demat accounts cannot directly access NDS-OM. As already announced in the First Bi-monthly Monetary Policy Statement, 2015-16, Reserve Bank is working, along with CCIL and depositories, to give demat account holders direct access to NDS-OM. This is expected to open up a large investor base, hitherto untapped, for investment in G-Sec. Even though G-Sec are globally institutional markets, this step is one of the most significant ones to facilitate retail investment in G-Sec.

IV. Integration at the depository level

35. Currently though intra-depository transfers of G-Sec take place seamlessly between two beneficiary owners within a depository, there is no facility to transfer G-Sec seamless across depositories. Further, at present, there is no linkage between the RBI SGL system and the depositories. As a result, transfer of securities between SGL and demat accounts involves a manual process. The manual process involves delays and inhibits seamless movement of securities between SGL and demat accounts. As announced in the First Bi-monthly Monetary Policy Statement, 2015-16, Reserve Bank is working along with the depositories to implement a seamless transfer of securities among depositories and RBI SGL which would effectively lead to an integrated depository system for G-Secs. This would greatly facilitate transaction on the exchanges between a SGL-account holder and non-SGL account holder.

V. New Products

36. Permitting introduction of new products in OTC as well as exchange traded space has always been a mutually consultative process between the Reserve Bank of India and the market participants. However, the approach adopted for introduction of interest rate options (IRO), I can, say, marks a fundamental departure. While the final guidelines are expected to be issued shortly, I can share that the guidelines would be truly principle-based and not prescriptive. It is proposed to permit a broad range of instruments including simple call and put options, caps, floors, collars and swaptions on both exchanges as well as in the OTC market. While the Working Group on Introduction of Interest Rate Options (Chairman: Prof. P.G. Apte) had recommended standardized contracts in the OTC market, the feedback received is that this may not be feasible. Another issue that has been flagged in the feedback relates to allowing users to hedge their foreign currency interest rate exposures using options on foreign currency interest rate benchmarks with Authorised Dealer banks in India on a back-to-back basis. This needs to be examined separately and may not be included as part of Rupee IRO guidelines.

37. Broadly, the same approach will be followed while finalizing guidelines on all new products - both OTC as well as exchange traded.

VI. Regulation of Electronic Platforms

38. Electronic platform trading has the benefits of improved transparency, reduced transaction times, efficient audit trails, improved risk controls and enhanced market monitoring. In the aftermath of the last financial crisis, internationally, there is a move to promote trading of financial instruments on electronic platform.

39. In India, as mentioned earlier, we can be considered pioneers in creating anonymous electronic platforms for trading. NDS-OM, an anonymous electronic platform for trading in Government securities was created a decade ago. Most trades in G-Sec now gets executed on NDS-OM. Similarly, 'Clearcorp Repo Order Matching System' (CROMS), an STP enabled electronic anonymous order matching platform to facilitate dealing in market repos in G-Sec is also available. The availability of electronic trading platform with robust clearing and settlement mechanism has been instrumental in the phenomenal growth observed in the outright and repo market in G-Sec.

40. Taking into account the experience of NDS-OM and CROMS in G-Sec, there is a need to introduce electronic trading dealing platforms for other financial instruments like corporate bonds, CPs, CDs and derivative products. Reserve Bank of India has also been receiving requests from various entities to introduce electronic platforms for these instruments. Accordingly, it is now proposed to prescribe a framework for authorization of electronic dealing platforms for financial instruments regulated by the Reserve Bank of India. The overarching philosophy behind the framework would be to permit more than one electronic platform subject to eligibility and demand. The transactions on such platforms could be piped to the related settlement agency for post-trade processing, etc.

VII. OTC Derivative Reforms

41. In response to concerns about systemic risks in over-the-counter (OTC) derivatives markets, the G-20 leaders agreed in 2009 to a comprehensive reform agenda to improve transparency in these markets, mitigate systemic risk, and protect against market abuse. All the jurisdictions, including the Emerging Market Developing Economies (EMDEs) have progressed substantially on the above as brought out in the last Financial Stability Board (FSB) progress report on implementation. Implementation is almost complete for trade reporting and higher capital requirements for non-centrally cleared derivatives. As observed in the Report, the authorities, however, continue to report challenges concerning the quality and completeness of the data being reported to Trade Repositories (TRs) and the ability to access, use and aggregate this data. FSB’s Thematic Review on OTC Derivatives Trade Reporting which came out in November 2015 identified several recurring issues that are posing challenges including concerns over data quality, capacity to effectively aggregate information across TRs, existence of barriers to reporting complete data to TRs, and barriers to authorities’ access to TR-held data.

42. From an EMDE perspective, the cross-border reporting and access to TR data has come out as a major issue which, as recommended, needs to be addressed legally. While the imperatives behind this are appreciated, their implementation would require navigating the existing privacy provisions nationally which may be challenging. As an alternative, to achieve early compliance, cooperative arrangements may also be considered pending legal frameworks. As the legislative process is usually long drawn and requires political support, the approach should not mandate legislative changes for all aspects of the reform agenda.

43. One of the biggest challenges for EMDEs remains meeting recognition/ equivalence requirements of major financial centres in OTC derivatives. While the concerns relating to uneven implementation of reforms may be an issue, forcing home country jurisdictional requirements onto host country entities, particularly financial market infrastructure entities could become a sensitive subject. From an EMDE perspective, this also comes in the way of achieving other objectives, such as, mandating central clearing for certain standardised OTC products. If the CCP is not recognised, participation of banks from other jurisdictions could be hampered affecting market development adversely. Some segments of the contributors to market liquidity may be forced to withdraw from the market thereby making the markets shallower. This could impact the longer term market development. This will also have an adverse impact on ability of market participants to hedge various risks using these derivative instruments.

44. Such an approach defeats the very purpose of an internationally-coordinated approach. Once any entity is recognised as compliant with the internationally accepted principles, subject to all the review mechanisms, additional bilateral requirements are difficult to justify. We are aware that the regulators in respective countries requiring this recognition are bound by the legal provisions in their jurisdictions but it is best to address such issues on a multi-lateral basis. The Report of the IOSCO Task Force on Cross-Border Regulation, which was published in September 2015, examined various issues comprehensively. There is an urgent need to agree on a broad set of equivalence principles internationally and not to insist on introduction of country specific requirements over other jurisdictions. Mutual reliance among the regulators within the framework of agreed global best practices and sound principles should be the ideal way to resolve avoidable frictions.

45. Beyond the above agenda, there are several other work-streams whose recommendations have a bearing on the functioning of the markets. For instance, the FSB work-stream on resolution of financial entities requires host country jurisdictions to allow bail-in clauses for all deposit liabilities raised by home country entities. The implications of such a sweeping mandate could be serious for the interests of domestic depositors. The challenge would be to strike a balance of the interest of various stakeholders.

46. In India, a Standing Committee under the Technical Advisory Committee (TAC) on Financial Markets has been constituted to assess, on a continuing basis, the implications of recommendations of various international standard setting bodies, through different work-streams, on domestic OTC markets. The Committee would also help in formulating appropriate policy response in this area.

VIII. Corporate Bonds

47. Based on recommendations of a Working Group set up under the aegis of FSDC-SC, certain measures have been announced in the Union Budget for 2016-17 for development of the corporate bond market:

-

Setting up of a dedicated fund to provide credit enhancement to infrastructure projects by the Life Insurance Corporation (LIC);

-

Issue of guidelines by the Reserve Bank of India to encourage large borrowers to access a certain portion of their financing needs through market mechanism instead of the banks;

-

Expansion of investment basket of foreign portfolio investors to include unlisted debt securities and pass through securities issued by securitisation SPVs;

-

Introduction of electronic auction platform for developing an enabling eco system for the private placement market in corporate bonds by SEBI for primary debt offer;

-

Development of a complete information repository for corporate bonds, covering both primary and secondary market segments; and

-

Development of a framework for an electronic platform for repo market in corporate bonds.

48. We are in the process of implementing the recommendations. In addition, certain other measures will be announced after finalization of the recommendations of the Committee.

49. Enactment of the Bankruptcy Act will be a defining event as regards the development of the corporate debt market. Some of the recommendations of the Companies Law Committee, particularly relating to private placement of securities, could also have far reaching implications for easing the issuance process. Another significant recommendation of the Committee is to exclude instruments covered under Chapter III D of the Reserve Bank of India Act, 1934 in the term ‘debenture’ as defined in Section 2 (30) of the Companies Act, 2013. This will provide the necessary clarity regarding issuance of CPs and other money market instruments.

IX. Use of Financial technology

50. Use of financial technology (fintech) in strengthening market infrastructure has been the buzzword in international fora. In particular, use of distributed ledger technology (DLT) holds a lot of promise for all transaction networks requiring non-repudiation and finality through maintenance of real time updated transaction ledgers. Conventional 'non-distributed' systems like payment systems and clearing/settlement systems use centralised ledgers. DLT achieves this in a decentralised manner while (i) keeping the identities of the participants unknown and (ii) without any central agency regulating the participants or the flow of transactions. Bitcoin represents one end of the applications spectrum of 'permissionless', completely decentralised transactions. Several applications are, however, being attempted across the spectrum, trying to marry the technology with the conventional centralised systems for efficiency gains.

51. While it may be premature to talk about regulating block-chains, there is need to continually engage with the industry to try to understand various applications being developed around the technology and monitor the developments in this space. The regulatory focus will be on identifying potential use cases, in close collaboration with the industry, where this technology could be leveraged. Controlled adoption in identified areas will be the preferred approach.

52. Towards leveraging the benefits of fintech, particularly block-chain technology, it would be our constant endeavour to engage with industry participants to explore the adoption of various innovations in strengthening market infrastructure. Concept papers exploring possible use cases of these technologies in the financial market infrastructure would be prepared and placed in public domain for wider feedback.

X. Role of FIMMDA

53. As a person who has been involved with the development of the debt market in India under various capacities, I can see the growing importance and role of FIMMDA in the fixed income and derivatives market. The consultations between the Reserve Bank of India and the FIMMDA, both formally and informally, on various issues of policy have not only helped us in understanding the point of view of the participants but have also entrusted greater responsibility on FIMMDA as a market body.

54. Today, apart from coming out with price valuations for G-Sec and non-G-Sec, FIMMDA has been given added responsibilities of developing and operating critical market infrastructure like reporting platform for corporate bonds, repo in corporate bonds, CPs and CDs. Further, FIMMDA has been appointed as the accrediting body for brokers in the OTC interest rate derivatives market. In the immediate future, FIMMDA will have a greater role to play in the rollout of CDS in India. This has widened the scope and responsibility of FIMMDA and it has been successful, so far, in fulfilling these responsibilities. Now it is time to reflect upon the past achievements and have a vision for the future. One such vision could be conferring SRO status to FIMMDA.

55. Changing nature of financial markets necessitate that organisations that are not from traditional regulatory structure participate in bringing orderliness in activities. Self-regulation is an important part of the regulatory structure of securities markets. Self-regulation and Self-Regulatory Organizations (SROs) are considered important in improving the effectiveness of securities regulation and market integrity. Use of SROs may lead to more efficient financial markets, thus enhancing businesses’ access to public equity and debt markets for accessing capital at a reasonable cost, which supports business expansion and economic development. The regulators designate SRO as a ‘competent authority’, to implement certain rules and regulations.

56. SROs exercise certain regulatory authority over an industry or profession, which could be in addition to existing Government regulations or fill the vacuum of absence of regulations. FIMMDA was created as a voluntary body for the interest rate market, and is a not-for-profit organization. The activities of FIMMDA and its role in the underlying market clearly indicate its self-regulatory role in the concerned markets and it could be termed as a “Quasi-SRO”. Certain activities typical of a SRO like prescription of Code of Conduct for members, oversight over brokers, and arbitration of disputes (in a limited way) are already being carried out by FIMMDA. Presently FIMMDA, through the Financial Benchmarks India Ltd (FBIL), is also part of benchmark administration which is vital to market integrity. There is, however, an urgent need for FIMMDA to strengthen itself and broaden its mission to carry out tasks commensurate with the developments in the market and the role envisaged by the Reserve Bank of India. In this regard, there is a need for active participation from all the members of FIMMDA, especially the public sector banks (PSB) who are major players in the banking/financial sector.

57. FIMMDA may have to play a more proactive and preeminent role and for this there is an urgent need to build competencies – both technical and financial, to undertake additional responsibilities as SRO. The focus needs to be on creating on robust organisational capabilities, by expanding its membership base, to undertake the functions for effective self-regulation within a broad framework of public accountability. I would suggest that FIMMDA draws up an action plan in this direction with clear goal posts to be achieved within appropriate time lines.

Conclusion

58. As laid out above, over the next few years, it can be expected that the Indian debt markets will evolve into a syncretic ecosystem connecting more varied investor classes alongside multiple platforms and trading venues with a seamless integration at the depository level. This will be achieved in a non-disruptive manner without radically disorienting the existing setup. The market infrastructure would also be greater aligned with the global reform process with greater role for innovative fintech.

59. As announced in terms of the Medium Term Framework for FPIs, the total investment by FPIs in G-Secs is expected to reach 5 per cent of the outstanding by March 2018. This, along with the additional space created for SDLs, is expected to create a predictable regime. Based on experience, the feasibility of gradually opening up certain segments/tenors fully in order to enable inclusion of Indian G-Sec in global bond indices could be a possibility.

60. With incremental opening up of the capital account and the increasing internationalization of Indian Rupee, greater play by global investors in onshore markets would become inevitable. The issue of guidelines for “Masala” bonds and agreeing to open up investment route for foreign investors through ICSDs all point in this direction. The effort would be facilitate this in a non-disruptive manner.

61. In conclusion, I would like to come back to the theme of intellectual openness in the context of changing role of institutions. I can do no better than quote from the a commencement address given by John W. Gardner in 1968 where he talks about the reasons for failure of institutions:

Twentieth century institutions were caught in savage crossfire between uncritical lovers and unloving critics. On the one side, those who loved their institutions tended to smother them in an embrace of death, loving their rigidities more than their promise, shielding them from life-giving criticism. On the other side, there arose a breed of critics without love, skilled in demolition but untutored in the arts by which human institutions are nurtured and strengthened and made to flourish. Between the two, the institutions perished.

62. It is in the spirit of this open debate that we, as critical lovers or loving critics rather than uncritical lovers or unloving critics, have to keep reassessing our institutional philosophy without disassociating ourselves from our core values. Keeping this spirit in view, I wish the ensuing sessions will see very high quality, open and productive discussions.

63. Thank you for patient listening.

|