Thank you for inviting me to deliver the first Ramnath Goenka lecture. As you know, Shri Goenka was a freedom fighter, who built the Indian Express into a national newspaper. In his time, it was arguably the best investigative newspaper in the country. He was instrumental in highlighting the excesses of the Emergency, which probably contributed to Indira Gandhi’s defeat when she lifted it. He continued to be a tireless scourge of corruption and government high-handedness, and was responsible for unsettling many a minister and business tycoon. It would be fitting in a lecture in his memory to speak about the efforts we are making in India today on increasing transparency and curbing corruption. However, I have said what I needed to on that elsewhere. Instead, I will speak today on India’s engagement with the global economy, and how best to manage it in these turbulent times

The global economy is finding it hard to restore pre-Great Recession growth rates – every report of the IMF seemingly downgrades its previous growth forecasts. Why has the recovery been so slow? The immediate answer is that the financial boom preceding the Great Recession left industrial countries with an overhang of debt, and debt, whether on governments, households, or banks, is holding back growth. While the remedy may be to write down debt so as to revive demand from the indebted, it is debatable whether additional debt fueled demand is sustainable. At any rate, large-scale debt write-offs seem politically difficult even if they are economically warranted.

But perhaps the debt overhang points to a deeper cause; the debt-fueled demand before the Great Recession, which has led to the debt overhang now, hid a fall in global potential growth, perhaps because of the difficult-to-understand consequences of population ageing across the industrial world, and the slowdown in productivity growth.

Structural reforms, typically ones that increase competition, foster innovation, and drive institutional change, are the way to raise potential growth. But these hurt protected constituencies that have become accustomed to the rents they get from the status quo. Moreover, the gains to constituencies that are benefited are typically later and uncertain. No wonder Jean-Claude Juncker, the former Luxembourg Prime Minister, said at the height of the Euro crisis, “We all know what to do, we just don't know how to get re-elected after we've done it!”

Instead, industrial countries are engaged in ever more aggressive monetary policy moves. This imposes tremendous risks on emerging markets like ours, as we are faced with surges of capital inflows one day when investors go into “risk-on” mode only to see outflows the next as they switch risk off. At the same time, overcapacity in competitor countries threatens some of our key industries.

What Should India Do?

What should India do in this environment where the international investor is manic depressive in his behavior and all countries are striving for extra growth? Importantly, when global growth is uncertain, we should make sure that our domestic environment promotes strong, sustainable, and stable growth. This requires a firm platform of macroeconomic stability. Let me elaborate.

The recent central budget emphasized fiscal prudence and adhered to past commitments, even while allocating resources towards capital spending and focusing on structural reforms, especially in agriculture. The subsequent fall in government bond yields suggests that market investors were calmed by the Government’s overall message. Fiscal consolidation, combined with lower commodity prices, has also led to a lower current account deficit.

Inflation is also clearly down since the days of double-digit CPI inflation not so long ago. The RBI’s inflation-focused monetary framework will be strengthened by the constitution of the monetary policy committee mooted in the Finance Bill. While the RBI Governor will no longer be able to set monetary policy unilaterally, I believe shifting the decision to a committee is in the economy’s interest. Not only will a committee aggregate multiple views better than an individual can, it will offer more continuity, and be less subject to undue pressure. I believe the monetary reforms of this Government will stand out as one of its signal achievements.

The last leg of the stabilization agenda is to clean up the stressed assets in the banking sector so that banks have the room to lend again. The problem in the past was that banks simply did not have enough powers to force promoters to pay, or to put stressed assets back on track. Unlike more developed countries, we do not have a functioning bankruptcy system, though a bill is currently before Parliament. Therefore, we first had to create an effective out-of-court resolution system. Having done that, we are now working with banks to recognize and resolve stressed assets, even while getting them to raise capital where necessary. Our intent is to have clean and fully provisioned bank balance sheets by March 2017.

Perhaps the hardest aspect of this stabilization agenda has been to persuade the economics commentariat of the need for macroeconomic stability when growth is below expectations. The constant call of the economic sirens, seeking to lure the economy onto the shoals of economic distress, is “Lord, give us stability, but not just yet!” Growth is always more important, no matter how the risks build up. Usually, the sirens call on you to not be doctrinaire (after all, only academic economists care about fiscal deficits), to be practical (does it really matter if an NPA is recognized a quarter or three later), and to appreciate Indian realities (everyone may say they hate inflation but no one really wants to bear the pain of the disinflationary process).

I believe we are in the process of proving the sirens wrong. Given the inhospitable world economy and two successive droughts in India, either of which would have thrown the economy into a tail spin in the past, our focus on macroeconomic stabilization must be part of the explanation why we have over 7 percent growth, low inflation, and a low current account deficit unlike some of our emerging market counterparts. Now, we have to build on this sound base. What will be particularly important is how we engage with the world economy. I want to talk specifically about trade, the exchange rate, capital flows, and ideas.

International Trade

For the first time in decades, global trade has consistently grown more slowly than global output. There are a number of possible explanations; as countries get richer, non-traded services constitute a greater fraction of GDP, causing GDP to grow faster than trade. Also, with trade-intensive capital goods’ investment muted because of global overcapacity, trade grows more slowly than GDP. Finally, as industrial countries become more competitive, and as China moves up the value chain, more of the inputs going into final products are being sourced from inside a country rather than from outside the country. Some global supply chains are therefore contracting. For all these reasons, the heady days when Indian trade in goods and services were expanding at a double digit pace will probably only be a memory for some time.

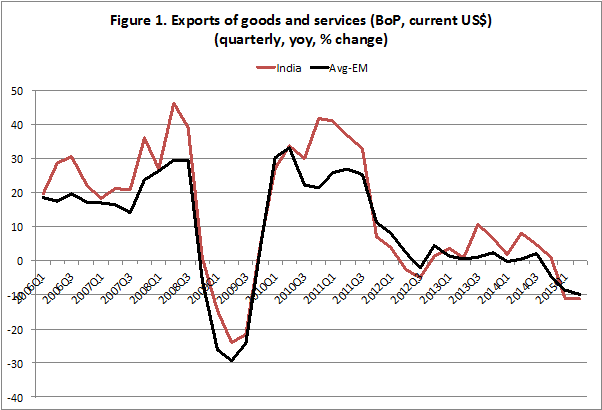

It is useful to examine recent trade data to see how India compares with rest of the world. Figure 1 suggests the growth of Indian exports of goods and services broadly mirrors that of emerging markets.

Source. IMF Balance of Payment Statistics. Emerging markets (EMs) include Brazil, China, Indonesia, Mexico, Russian, South Africa, Thailand, Turkey, and India. The black line shows a simple average of growth rates across these EMs.

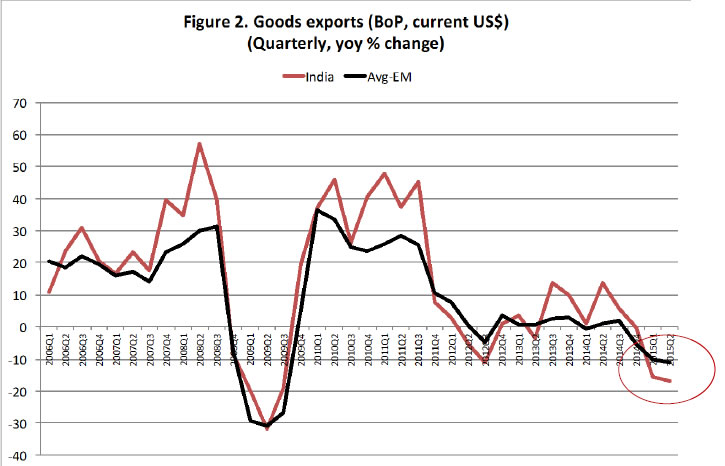

Most recently, of course, emerging market commodity exporters have been hit by lower prices. Nevertheless, Indian goods exports seem to be doing worse recently than goods exports from emerging markets (see figure 2).

Source. IMF Balance of Payment Statistics. Emerging markets (EMs) include Brazil, China, Indonesia, Mexico, Russian, South Africa, Thailand, Turkey, and India. The black line shows a simple average of growth rates across these EMs.

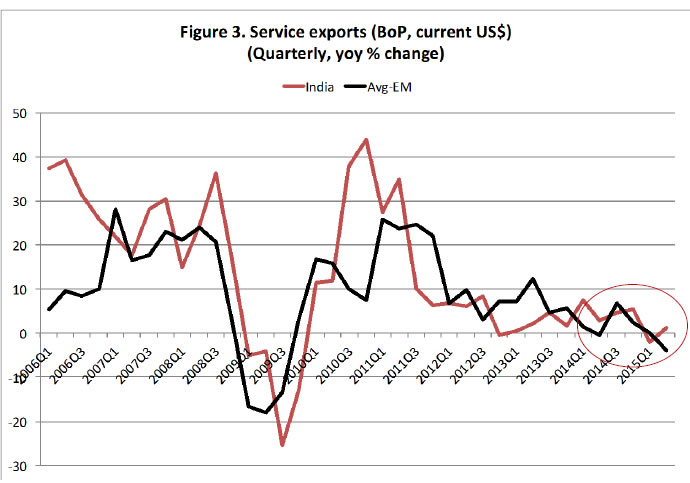

At the same time, the growth of Indian service exports seems to be doing somewhat better, perhaps because countries like the United States that we export services to are recovering more strongly. Of course, these differences are over very short periods, so it is probably unwise to draw strong conclusions from them. What one can probably take away is that India is not alone in suffering a fall-off in trade.

Source. IMF Balance of Payment Statistics. Emerging markets (EMs) include Brazil, China, Indonesia, Mexico, Russian, South Africa, Thailand, Turkey, and India. The black line shows a simple average of growth rates across these EMs.

However, as Indian trade slows, industry bodies are urging authorities to do something. Of course, if all countries are experiencing slower trade, the remedies may be beyond the control of Indian authorities. While we can examine possible dumping in certain industries, we have to be careful that any remedies that increase prices in the protected industry do not render other domestic industries uncompetitive.

It is at these times of slowing trade that our pundits look at the exchange rate and argue it is overvalued. Of course, I have just argued that we are not alone in experiencing a fall in trade, but let us examine the exchange rate.

The Exchange Rate

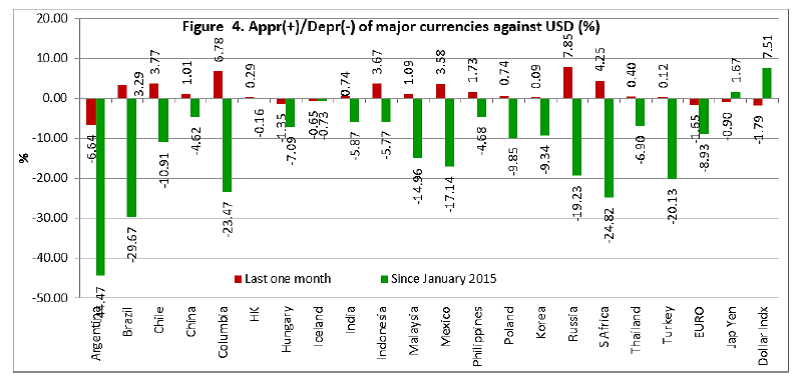

When most people think about the exchange rate, they think of the rupee’s value against the dollar. As Figure 4 indicates, the rupee seems to have weakened by about 6% against the dollar since the beginning of 2015, approximately the time our relative underperformance on goods exports started. This depreciation should have helped our exports, though the effects of depreciation show up only after a lag.

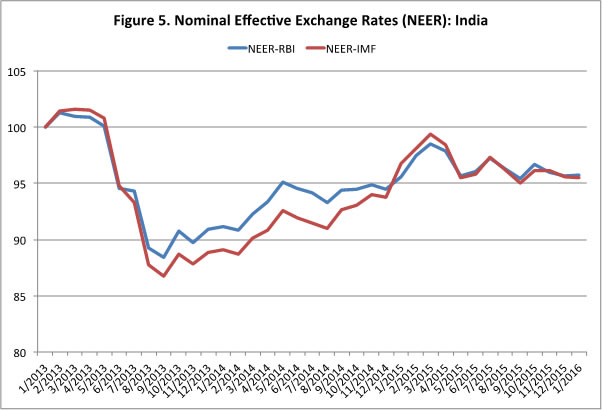

But we should note that other currencies have depreciated against the dollar also. So while we have gained an advantage versus US producers, other foreign producers may have become even more competitive because their exchange rate has depreciated more. Economists therefore advise looking at an index of the nominal effective exchange rate, which compares the rupee’s value versus other exchange rates, weighing each by their share in trade.

Sources. RBI and IMF. The indices are normalized to January 2013=100. An increase denotes an appreciation.

By this metric in Figure 5, the rupee has remained relatively flat since early 2015. What we have given up against the dollar, we have gained against the Euro or the Real, so overall, in trade-weighted terms, the rupee has been flat.

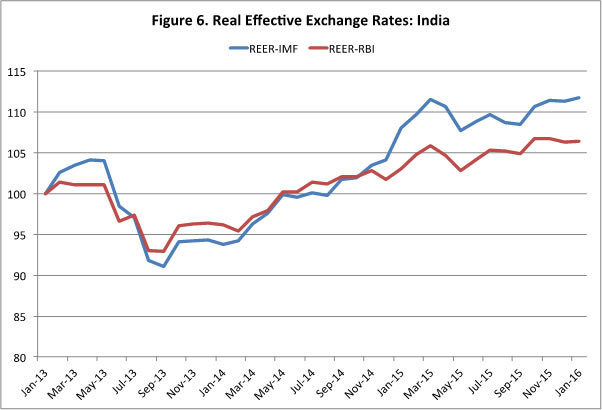

But wait a minute, our economist friends will say. Inflation in India is higher than inflation in most other countries. This affects competitiveness. If a widget cost a dollar to make a year ago in the United States, and ₹ 63 in India then, the Indian producer would have been competitive with the United States because the dollar was worth ₹ 63. But if inflation in India is 5% and zero in the United States, it would cost the Indian manufacturer ₹ 66.2 to make it today. If the rupee stayed at ₹ 63 to the dollar, the Indian manufacturer would have become uncompetitive today – the US producer would be able to manufacture the widget at a cost equivalent of ₹ 63 only. In other words, to retain competitiveness, the rupee has to depreciate by the inflation differential vis a vis a trading partner. An index of how competitive we are is called the “real effective exchange rate”. Think of that as the nominal effective exchange rate adjusted for inflation. The higher it is, the less the exchange rate has depreciated to offset inflation, and the more uncompetitive we are.

Sources. RBI and IMF. The indices are normalized to January 2013=100. An increase denotes an appreciation.

Figure 6, where I plot the real effective exchange rate, shows the age old truth that interpretation is in the eyes of the beholder. If a columnist wants to blame the exchange rate for our export slowdown, she can look at the index from the low point of September 2013 and argue it has appreciated 20% (based on the IMF measure). Of course, it would be hard to argue that the low point our exchange rate reached in September 2013 represented an equilibrium rate. Moreover, our exports were doing quite well relative to emerging markets for much of that period (see Figure 1).2 Indeed, over the last year when goods exports have slowed, the real effective exchange rate has been rather flat. So someone who wants to absolve the exchange rate of blame will point to the recent period.

But there is another reason to absolve the exchange rate of accusations of overvaluation. The real exchange rate is only one measure of competitiveness. Productivity also matters. In a rich country, firms are already at the productivity frontier, so they typically can improve productivity only through innovation. In a poor country, productivity can be improved simply by reducing existing bottlenecks or by moving a little closer to the productivity frontier through the adoption of already-known best practices. Productivity in India, for example, can improve simply if a better road is built from a factory to the rail head, or if the firm manages its inventories better. One reason Indian manufacturing GDP has been growing so fast when firms have been experiencing little increase in final sales is that firms have been focusing on improving productivity. So offsetting any rise in the real exchange rate is any productivity differential we enjoy with respect to the rest of the world. Assuming conservatively that this is about 2 percent a year, much of the real appreciation that economists complain about is offset by productivity differentials.

The bottom line is that even though Indian trade has been slowing, the slowdown is similar to what has been happening elsewhere, with a significant portion due to a fall in commodity prices, and a smaller share due to a fall in trade volumes. While goods exports may have suffered a little more over the last year, it is too early to discern a clear pattern, and certainly hard to pin the slow down on the exchange rate.3

The Goldilocks Rate

It is worthwhile to push this discussion a little further though. If the RBI could press a button and get the exchange rate it desired (as some economists imagine is possible) should it aim for a strong rupee or a weak rupee? Non-economists typically advocate a strong rupee – not only does it convey national strength, but you can buy more stuff with your rupee when you go abroad, and imports are cheaper. The non-economist is consumer focused.

Of course, it is precisely because domestic tourism and domestic production are disadvantaged relative to tourism abroad and foreign production that many economists prefer a weak rupee. Yet these modern day, producer-focused, mercantilists do not acknowledge that undervaluation is a subsidy to domestic producers paid for by domestic consumers and savers. The domestic consumer pays too high a price for foreign goods, and interest rates have to be kept artificially low so as to reduce the cost of holding the enormous foreign exchange reserves built up through intervention. There are costs over the long run also. A sizeable portion of the investment made in the country based on an artificially low exchange rate will turn out be uncompetitive when the exchange rate normalizes. One might argue that this reflects the experience of Japan in the 1990s and possibly the experience of parts of Chinese industry today.

An undervalued exchange rate might have made sense in the past for countries that had weak firms and small domestic markets. India is in a very different position today from the export-led East Asian tigers when they embarked on their growth path. The ideal exchange rate for us is neither strong nor weak, it is just right. Typically, market forces get you to this Goldilocks rate. Yet there are circumstances where rapid capital inflows or outflows can move the rate to a level that is unlikely to be supported by fundamentals. While the RBI would not claim to know precisely what the equilibrium level of the exchange rate is at any given point in time, we intervene to moderate adjustment whenever we believe the movement is extreme, driven by sentiment, and likely to be reversed. Our intent is to prevent overshooting and undue volatility, rather than to stand in the way of the needed adjustment.

Of course, temporary irrationality in the market can overwhelm a central bank. Much like a bank run, a falling currency can prompt further fall as foreign investors attempt to get out before they lose everything. To maintain orderly movement of the rupee versus other currencies, we believe we need three ingredients. First, good policies that ensure macroeconomic stability and convinces investors their money is safe over the medium term. I have already discussed this earlier.

Second, we should focus on attracting stable capital flows that will stay for the long run. This means resisting the temptation to open up too much to short-term- as well as foreign currency denominated debt flows in good times, no matter how low an interest rate they charge. In the last few years, we have limited foreign portfolio debt investment in short term rupee debt instruments. It is not that these investors cannot sell long term bonds and leave at a moment’s notice, it is that investors in longer maturity bonds are likely to be a little more stable than investors who want overnight exposure only. At the same time, we have steadily expanded investment limits for foreign investors in government bonds, and will continue doing so.

Our new External Commercial Borrowing rules encourage infrastructure projects and other projects that have limited foreign earnings to either issue rupee Masala loans, or to borrow really long term tenors. This limits the risk that they will be required to repay when the exchange rate has moved adversely against them.

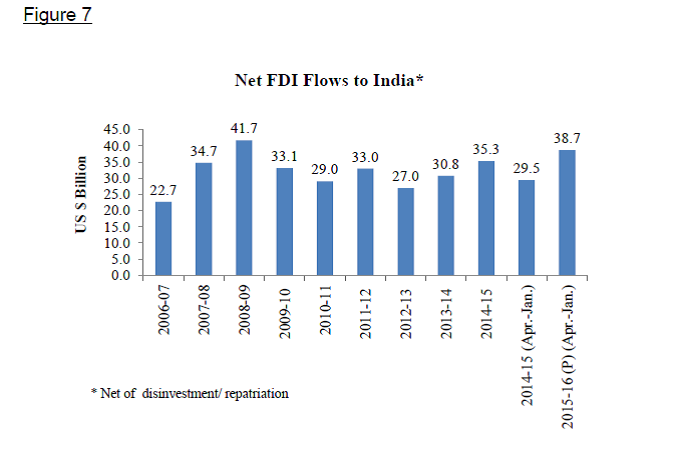

Finally, the Government has been encouraging foreign investors to “Make in India”. One offshoot of this campaign has been a sizeable rise in foreign direct investment, the most stable sort of investment. With two months left in the year to go, net FDI is already at the second highest level ever, and comfortable higher than the current account deficit.

The bottom line is that our policy towards foreign capital flows is one of steady liberalization, where we try and not be tempted by cheap finance, but draw in the risk-bearing capital we need to finance our growth. We intend foreign investors to get decent returns and we do intend to continuously ease both entry into and exit from the country.

Finally, our third line of defence is our foreign exchange reserves. We intervene in the exchange markets to smooth volatility, and typically find ourselves buying dollars at certain times and selling dollars at others in any given year.

How to increase exports

So if the exchange rate is unlikely to be a helpful tool in our quest to increase what we make in India, how should we export more? The answer is simple – improve productivity by building out infrastructure; improve human capital with better schools, colleges, vocational and on-the-job training; simplify business regulation and taxation; and improve access to finance. Fortunately, all this is what the government is focused on.

I am often asked, “What industries should we focus on, what should we encourage?” Learning from our past, I would say let us not encourage anything; that might be the surest way of killing it. Instead, let us make sure we create a good business environment that can support any kind of activity, and then let our myriad entrepreneurs figure out what new and interesting businesses they will create. In the 1990s, the IITs that Pandit Jawaharlal Nehru created to supply engineers to the commanding public sector heights of the economy instead supplied managers and programmers to body shops focused on dealing with the Y2K bug. These in turn evolved into our world-beating software giants. While the government did not create the software industry, it was not inconsequential by any means to its emergence and development. Similarly, let us enable business activity but not try and impose too much design on it.

Ideas and Analysis

Before concluding, let me emphasize one additional area of engagement with the world, ideas and analysis. Today, we have a seat at most international tables, many countries want to draw us into bilateral and multilateral treaties. When we were unimportant, we used to rail against the proposals that were inimical to us, knowing it would not make an iota of difference. As we get more power, we need to develop the capability of using it effectively.

Today, it is an unfortunate reality that international meets are still dominated by the old powers. But it is less through brute power politics and more through the power of ideas, agenda setting, and organization that they dominate. Agendas in the G-20 are still largely set by elements of the old G-7, and often we find that they have already agreed on their preferred approach. It is only when the big powers disagree that the rest of us have some hope of influencing outcomes.

The fault is not in the power structure, it is in us. Unless we amongst the emerging world put forward our agenda, build the intellectual and analytical basis for pushing it, and create coalitions to support it, we will have no chance of moving forward. Encouragingly, the BRICS do discuss policy issues and try and develop common approaches, but we need to do more. We also need to build coalitions with sympathetic industrial countries. In India, we need to build capacity in our think tanks and universities to inform our policy makers on how to approach and shape the international policy agenda. We need to be well prepared when we negotiate bilateral and multilateral treaties, so that we do not wake up too late to the fact that we have given away the house with little in return. With careful analysis, engagement, and coalition building we will be able to influence the global agenda, and will stop being seen as an obstructionist but ultimately powerless country that we may have been in the past.

Conclusion

Let me conclude. Shri Ramnath Goenka focused on unearthing facts that would help move the public debate forward. All too often, our public debates generate more noise than illumination, and we should learn from the example he set. As we cope with the global slowdown, and as we frame our policies going forward, we need to debate what our policy path will be, based on facts, empirical analysis, and sound arguments. I have laid out a view. I look forward to alternative viewpoints. Thank you for listening to me.

|