I am happy to be addressing this first ever CII Summit on Non-Banking Financial Companies (NBFCs) to deliberate on “Regulatory Paradigm & Contours of Growth – Vision 2020”. The context in which such a Summit has been organised is also very apt. World over, there is an awakening, post the great financial crisis of 2008, about the existence, contribution, magnitude, significance and risks of non-banking financial sector. From a benign neglect of or indifference to this sector, either by default or by deliberate choice, the world has now become anxious and seriously concerned about it. This awakening has resulted in enhanced attention, monitoring and regulation of this sector. Therefore, it is very apt that the sector has also noticed it and desires to seriously discuss its prospects in the changed scenario and realign itself with a renewed vision.

Global Shadow Banking Monitoring Report of FSB - 2015

2. The Financial Stability Board (FSB), came into existence post financial crisis, when the Leaders of the G20 countries decided to convert the then existing Financial Stability Forum into FSB to address vulnerabilities and to develop and implement strong regulatory, supervisory and other policies in the interest of financial stability. The FSB has been monitoring the shadow banking sector closely for the past five years and publishing its monitoring report. I will like to highlight some of the key findings from its latest report, as they will provide a worthwhile background setting for your deliberations today.

3. The 2015 Report of the FSB presents the results of the fifth annual monitoring exercise using data as of end 2014 for 26 jurisdictions, which together account for about 80% of global GDP and 90% of global financial system assets. The report includes the results of the macro-mapping, including size and growth trends of the Monitoring Universe of Non-banking Financial Institutions (MUNFI) estimate, cross-jurisdiction analysis, trends in sub-sectors and interconnectedness with the banking system. It also discusses a narrower measure of shadow banking, which is constructed by filtering out non-bank financial activities that have no direct relation to credit intermediation (e.g. Equity Investment Funds) or that are already prudentially consolidated into banking groups. As a result, it is believed that this narrower measure more accurately reflects the size and composition of the shadow banking sector, subject to the caveats and FSB’s resolve to further refine the narrower measure. Another change that has been brought in this time around is a new activity-based “economic function” measure of shadow banking, each of which involves non-bank credit intermediation that may pose shadow banking risks (e.g. maturity / liquidity transformation and leverage). The five economic functions are certain entities that are susceptible to runs (EF1), lending dependent on short-term funding (EF2), market intermediation dependent on short-term funding or secured funding of client assets (EF3), facilitating credit creation (EF4), and securitisation-based intermediation (EF5).

4. The main findings from the latest exercise are as follows:

The Narrow Measure

-

The narrow measure of global shadow banking that may pose financial stability risks amounted to $36 trillion in 2014 for the 26 participating jurisdictions. This is equivalent to 12% of financial system assets, and has grown moderately over the past several years.

-

More than 80% of global shadow banking assets reside in a subset of advanced economies in North America, Asia and northern Europe.

-

The new classification by economic functions shows that credit intermediation associated with collective investment vehicles with features that make them susceptible to runs (e.g. money market funds (MMFs), hedge funds and other investment funds) represents 60% of the narrow measure of shadow banking. It has grown more than 10% on average over the past four years. By contrast, the level of securitisation-based credit intermediation – among the key contributors to the financial crisis – has fallen in recent years.

-

At the aggregate level, interconnectedness between the banking and the non-bank financial system continues to decrease from its pre-crisis peak.

The Broad Measure

-

An aggregate “MUNFI” measure of the assets of other financial intermediaries (OFIs), pension funds and insurance companies grew by 9% to $137 trillion over the past year, and now represents about 40% of total financial system assets in 20 jurisdictions and the euro area.

-

In aggregate, the insurance company, pension fund and OFI sectors all grew in 2014, while banking system assets fell slightly in US dollar terms.

-

While non-bank financial intermediation shrank somewhat immediately following the financial crisis, it has been rising over the past several years. OFI assets in the 20 jurisdictions and the euro area reached 128% of GDP in 2014, up 6 percentage points from 2013 and 15 percentage points from 2011. It is nearing the previous high-point of 130% prior to the financial crisis.

-

Emerging Market Economies (EMEs) showed the most rapid increases in OFI assets. In 2014, 8 EMEs had OFI growth rates above 10%, including two that grew over 30%. However, this rapid growth is generally from a relatively small base.

-

Among OFI sub-sectors that showed the most rapid growth in 2014 are trust companies, MMFs, and fixed income and other funds. Trust companies (mostly based in China) continued to experience growth of 26%, similar to the past several years. Perhaps more surprisingly, MMFs experienced 20% growth in 2014 (largely driven by some euro area jurisdictions and China), following low or negative growth in the prior three year period. Fixed income funds and other funds grew approximately 15% in 2014.

-

It should be noted that hedge funds remain underestimated in the FSB’s exercise due to the fact that a portion of international financial centres (IFCs), where a number of hedge funds are domiciled, are currently not within the scope of the exercise.

Shadow Banking in India

5. While the world generally refers to this sector as ‘shadow banking sector’, we have been calling it as the ‘non-banking financial sector’. Further, while the world has, as I said, now sat up and perked its collar to look at this sector intensely, India had understood the sector’s relevance and the risks that it may pose, way back in early 1960s itself, when, in 1963, Chapter III B dealing with regulation of the Non-Banking Financial Institutions was added to the Reserve Bank of India Act 1934. It recognised that non-banking financial activity is an integral part of the financial system and complements commercial banking; only that appropriate vigilance and due-diligence will be needed to regulate this sector.

NBFC Regulation

6. In a free economy, economic agents are primarily free to undertake any economic activity. In their normal course, they will be aspiring for continuous growth. However, certain economic activities have, as we all know, greater externalities and financial sector is one where the externalities are such that it warrants close regulation and supervision in the interests of systemic stability, safety and soundness of banks and other financial institutions and to protect the consumers. The objective of NBFC regulations during the twentieth century was predominantly to protect the interests of the depositors. However, as the NBFCs grew in size and their interconnectedness with the banking system became visible and raised concerns about their capacity to disturb systemic stability, the NBFCs were brought under prudential regulatory framework from 2006 onwards.

7. While the overall approach followed the contours as described above, the Reserve Bank, as the regulator of NBFCs has kept the sector’s potential to contribute to the development of identified segments of the economy and accordingly has been following a developmental bias in its regulatory framework relating to the NBFCs. The NBFCs focus on niche areas of business addressing specific needs of customers. Therefore, the Reserve Bank has classified varieties of specific types of NBFCs separately and regulates each such type differently. As on date such types include asset financing, core investment, loan, investment, micro-financing, factoring, infrastructure financing, mortgage guarantee, etc. activities. Further, the housing finance, insurance and collective investment activities, though statutorily defined as NBFI activities, their regulations have been left in the hands of other sectoral regulators like the National Housing Bank (NHB), the Insurance Regulatory and Development Authority (IRDA), the Pension Fund Regulatory and Development Authority (PFRDA) and the Securities and Exchange Board of India (SEBI).

8. This approach reflected the position that non-bank financial system may contribute to financial deepening in these identified segments. The NBFCs can be advantageous due to their ability to lower transaction costs, quick decision making capabilities, customer orientation and prompt provision of services. In terms of products and services offered, the NBFCs complement the banks.

9. Nevertheless, the business model of NBFCs is inherently risk-prone. Weaker underwriting standards, enhanced risk taking capabilities and increased complexity of their activities cause concerns.

10. Besides riskiness pertaining to business model, NBFCs are exposed to key risks emanating from regulatory gaps, arbitrage and contagion effect. NBFCs are more prone to systemic risks on account of concentration of exposure to specific sectors. Also, since these entities are more dependent on bank funding, both directly and indirectly, the interconnectedness risk tends to be higher. Their asset-liability mismatches accentuate liquidity risks. All told, these risks can quickly escalate as solvency risks and lead to systemic risk as well.

11. Therefore, careful and continuous monitoring is still required to detect any increases in systemic risk factors (e.g. maturity and liquidity transformation, and leverage) that could arise from the rapid expansion of credit provided by the non-bank sector. Reserve Bank has been dynamically making the regulatory framework suitable for the day. Certain changes in the framework brought in the last year or so deserve some recollection.

Recent NBFC Regulations

12. Changes to the regulations concerning NBFC sector over the last decade and a half had largely been incremental. However, in November 2014, a detailed review of the entire regulatory framework for the NBFC sector was undertaken with a view to transitioning, over time, to an activity based regulation of NBFCs as opposed to the current approach of entity-based regulation. The Bank has been mindful of the fact that the revisions should not impede the dynamism displayed by NBFCs in delivering innovation and last mile connectivity for meeting the credit needs of the productive sectors of the economy. The broad principles followed in framing the revised guidelines was to review the regulations from the perspective of the mandate of the Reserve Bank, viz., financial stability, depositor protection and customer protection. Hence, a) the focus has been on addressing risks where they exist, b) address gaps in regulation, c) reduce complexities and make regulations simple and easy to follow, d) harmonise regulations within the sector and with that of banks to a limited extent, e) acknowledge that there may be pockets within the sector that do not require to be stringently regulated and f) give adequate time to the NBFCs to adjust to the revised regulatory framework so that there are no disruptions in business.

13. Consequently, the revised regulatory framework for NBFCs was introduced and the threshold for systemic significance has been revised to total asset size of ₹ 500 crore. Now, there are two broad categories of NBFCs requiring closer attention of regulators and supervisors. These are a) non - deposit accepting NBFCs with asset size of less than ₹ 500 crore (NBFCs-ND) and b) non - deposit accepting NBFCs with assets of ₹ 500 crore and above (NBFCs-ND-SI) and deposit accepting NBFCs (NBFCs-D). Reporting and regulatory provisions are accordingly applied to have better focus on systemically important entities and efficient allocation of supervisory resources.

14. Minimal prudential regulations have been prescribed for non-deposit accepting NBFCs with asset size of less than ₹ 500 crore. For these non-deposit accepting companies (NBFCs-ND) below the threshold of systemic significance, prudential regulations, other than capital adequacy and credit concentration norms, are applicable only where public funds are accepted and conduct of business regulations (FPC, KYC) where there is customer interface. A simple leverage ratio of 7 has been put in place so that their asset growth is in sync with the capital they hold. Further, reporting by such NBFCs will be through asimplified annual return. However, registration under Section 45 IA of the RBI Act is mandatory and they are subjected to a simplified reporting system along with minimum net owned funds (NOF) of ₹ 2 crore.

15. For those non-deposit accepting companies (NBFCs-ND-SI) above the threshold of systemic significance and for all NBFC-D, prudential regulations are applicable and conduct of business regulations wherever customer interface exists. In line with international best practices, core capital requirement has been strengthened (existing 7.5%; raised to 10% to be phased over 2 years). Asset classification norms have been aligned with that of banks (from the current 180 day and 360 day norm for loan and HP / Leased assets respectively to a 90 day norm phased in over 3 years). Higher standard asset provisioning has been put in place (0.4% against the existing 0.25% phased in over 3 years). Further, credit concentration norms have been harmonised between the various categories of NBFCs by removing the dispensation given to AFCs to exceed the defined norms by 5%. (Dispensation given to IFCs and IDFs has been retained as infra loans are high value loans) and corporate governance standards, viz., fit and proper criteria for directors, disclosure and transparency have been strengthened so that they are professionally managed and develop a sound compliance culture.

16. In order to harmonise the deposit acceptance regulations across all deposit taking NBFCs (NBFCs-D) and move over to a regimen of only credit rated NBFCs-D accessing public deposits, existing unrated Asset Finance Companies (AFCs), which were permitted to accept deposits, shall have to get themselves rated by March 31, 2016. Further, the limit for acceptance of deposits has been reduced for rated AFCs from 4 times earlier to 1.5 times of NOF.

17. The Principal Business Criteria (PBC) for NBFC-Factors has been revised to 50:50 from the existing 75:75, thereby aligning it with the provisions of the Factoring Regulation Act, 2011. Consequently, an NBFC whose factoring assets and factoring income are 50 percent of the total assets and total income respectively are now classified as NBFC-Factors. This is expected to provide a boost to factoring activities in the country.

18. In the case of NBFC- MFIs , based on recommendations of the Committee on Comprehensive Financial Services for Small Businesses and Low Income Households (Chairman: Dr. Nachiket Mor), the limit on the total indebtedness of a borrower was raised to ₹ 1,00,000/- from ₹ 50,000/-. Income criteria of borrowers for loans to be included as qualifying assets of these NBFCs was changed: for borrowers with a rural household annual income not exceeding ₹ 1,00,000/- against ₹ 60,000/- earlier and urban and semi-urban household income not exceeding ₹ 1,60,000/- against ₹ 1,20,000/- earlier; ceiling on the amount of loan that can be disbursed was revised to ₹ 60,000/- from ₹ 35,000/- earlier in the first cycle and ₹1,00,000/- from ₹ 50,000/- earlier in subsequent cycles. The income generating loan component has been reduced from 70% to 50%. Further, the Bank has also raised the loan limit, requiring a mandatory tenure of 24 months, to ₹ 30,000/- from ₹ 15,000.

Growth of the NBFC Sector

19. Total number of NBFCs have come down from 51,929 in 1997 to 11,769 as on September 30, 2015 whereas the asset size has grown from ₹ 75913 crore as at end March 1998 to ₹ 16,10,729 crore at end September 2015. Share of NBFC assets as a percentage of scheduled commercial banks’ assets has increased from 7% in 1998 to 14.8% in March 2015. There are 202 NBFCs-ND-SI (assets size ₹ 500 crore and above) with a total asset size of ₹14126 billion. The number of deposit taking NBFCs, including Residuary Non-Banking Finance Companies (RNBCs), decreased from 1,420 in 1997-98 to 209 in September 2015. Share of NBFC deposits as a percentage of scheduled commercial banks’ deposits has come down from 3.34% in March 1997 to 0.30% in March 2015.

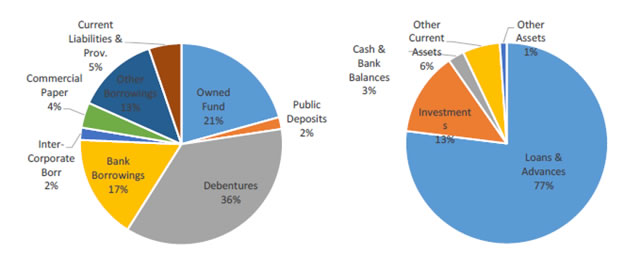

20. Sources and Uses of Funds of NBFC Sector–

Position As on September 30, 2015

21. Loans and advances extended by NBFCs-ND-SI posted strong double-digit growth of 15.5% during 2014-15, in contrast to the slowdown in commercial bank’s non-food credit during the same period (Chart 4.6). Strong growth in credit extended by the infrastructure finance companies, microfinance companies and loan companies contributed to sturdy growth in the loan portfolio of NBFCs-ND-SI. Among the sectors, infrastructure, medium and large-scale industries, and the transport sectors contributed to strong growth in credit off-take of the NBFCs-ND-SI. During 2014-15, NBFCs-ND-SI raised funds mainly through debentures and commercial papers. Borrowings from banks, which earlier constituted to be the main source of funding, has been progressively reduced. A notable feature is the rising exposure of mutual funds to the financial instruments floated mainly by the NBFC-Infrastructure Finance Companies (IFCs), Loan Companies (LCs) and NBFC-Micro Finance Institution (NBFC-MFIs).

22. In recent years, asset quality of NBFC sector has gone through the vicissitudes of overall deterioration spreading across the financial system as the economy slowed. Gross NPAs as per cent of credit deployed rose to 4.1 per cent by end-March 2015.

Prospects

23. In my opinion, the prospects for the sector in the medium term are not going to be uniform. Different segments of the sector are poised for different prospects and challenges.

24. For example, the NBFC-MFI segment is going to shrink heavily as the big ten of them convert themselves into Small Finance Banks in the next one year or so. I will hasten to add that this can yet bring higher impetus for the other NBFC-MFIs to grow, not just because of the availability of space vacated by the big ten, but also because the capital that will be released when many of the converting NBFC-MFIs pay off the current investors as a part of capital restructuring, and because of renewed interests by such venture capital aiming growth prospects in such conversions in the future.

25. The infrastructure NBFCs will have greater scope in the coming years, both because the economic growth will bring forth new projects and banks, having learnt lessons in the recent past, will have a restrained approach towards such projects. If the Infra-NBFCs will have their structuring these projects in a careful way, they will have good prospects.

26. As the large exposure regime for the banks will apply by 2018, NBFCs will have space for market funding or loan funding of big corporate financing in the medium term.

27. Loan companies will face enhanced consumer protection measures. They will be required to appropriately educate their workforce in selling right.

28. Investment companies will have bright prospects, as the equity and corporate bond markets expand, along with economic growth and careful recalibration of bank finance in the wake of Basle III.

Regulation - The Way Forward

29. At present, there are several categories of NBFCs and regulations vary across these NBFCs. The Committee on Comprehensive Financial Services for Small Businesses and Low Income Households (Chairman: Dr. Nachiket Mor) had recommended merger of various categories of NBFCs, into two viz., NBFCs and Core Investment Companies (CICs) and moving towards activity based regulation. The regulatory framework, put in place in November 2014, is a first step in this direction. Going forward, we will work towards greater harmonisation of the regulations with a view to reducing the number of NBFC categories.

30. However, the Reserve Bank is alive to the developmental needs of the economy and therefore will continue to approve of new types of NBFCs if the economy will need them. One such is NBFC-Account Aggregator (NBFC-AA) about which the Reserve Bank announced on July 02, 2015. The NBFC-AA will provide a technology enabled solution to a person to view at one place the position of his financial assets across institutions under different sectoral regulators. The guidelines for the same are under preparations.

31. Also, the Reserve Bank is actively studying the Peer-To-Peer lending arrangements that are slowly gaining traction. While recognising the need for innovative products and services, we should be conscious about the risks that may emanate out of such innovations. Based on the detailed study, we intend to bring out a Discussion Paper for public consultation.

32. There are demands that the regulations relating to the Core Investment Companies need revisiting. This is a work-in-process.

Conclusion

33. To conclude, I can only quote what the FSB concluded in its 2015 Report.

“Intermediating credit through non-bank channels can have important advantages and contributes to the financing of the real economy, but such channels can also become a source of systemic risk, especially when they are structured to perform bank-like functions (e.g. maturity and liquidity transformation, and leverage) and when their interconnectedness with the regular banking system is strong. Appropriate monitoring of shadow banking and the application of appropriate policy responses, where necessary, helps to mitigate the build-up of such systemic risks”. The Reserve Bank remains committed to such an approach.

|